| Index | Q2 2023 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 1.1% | 5.7% |

| S&P 500 (US$) | 8.7% | 16.9% |

| S&P 500 (C$) | 6.4% | 14.3% |

| MSCI EAFE (US$) | 3.0% | 11.7% |

| MSCI EAFE (C$) | 0.7% | 9.2% |

| FTSE TMX Universe Bond Index (C$) | ‐0.7% | 2.5% |

| C$ / US$ | 1.3533 to 1.3240 (2.2%) | 1.3544 to 1.3240 (2.3%) |

* Index returns are total returns, including dividends.

A RUSH TO AI

In 1848, American pioneer James Marshall discovered gold at Sutter’s Mill, igniting the great California Gold Rush. Droves of amateur and professional prospectors from around the globe ventured to California hoping to claim their piece of the wealth. As a result, the immediate vicinity became overcrowded, even though a more valuable deposit lay in wait a mere 350 km away for someone to uncover. All they had to do was look.

There are many similarities that can be drawn between the California Gold Rush and recent market history. In the past three years, news headlines have created similar eagerness around software‐as‐a‐service (SaaS) subscription models, the Cloud, Cryptocurrency, Blockchain, non‐fungible tokens (NFTs), and most recently generative Artificial Intelligence (AI). In each case, the market reaction to the latest trend eventually cooled, eclipsed by the next new thing. Today, once again, the stock market is piling into a handful of companies on the forefront of a new technology which is driving the entire S&P 500 higher. This time the action is fueled by the hopes that generative AI will provide notable improvements to productivity and innovation.

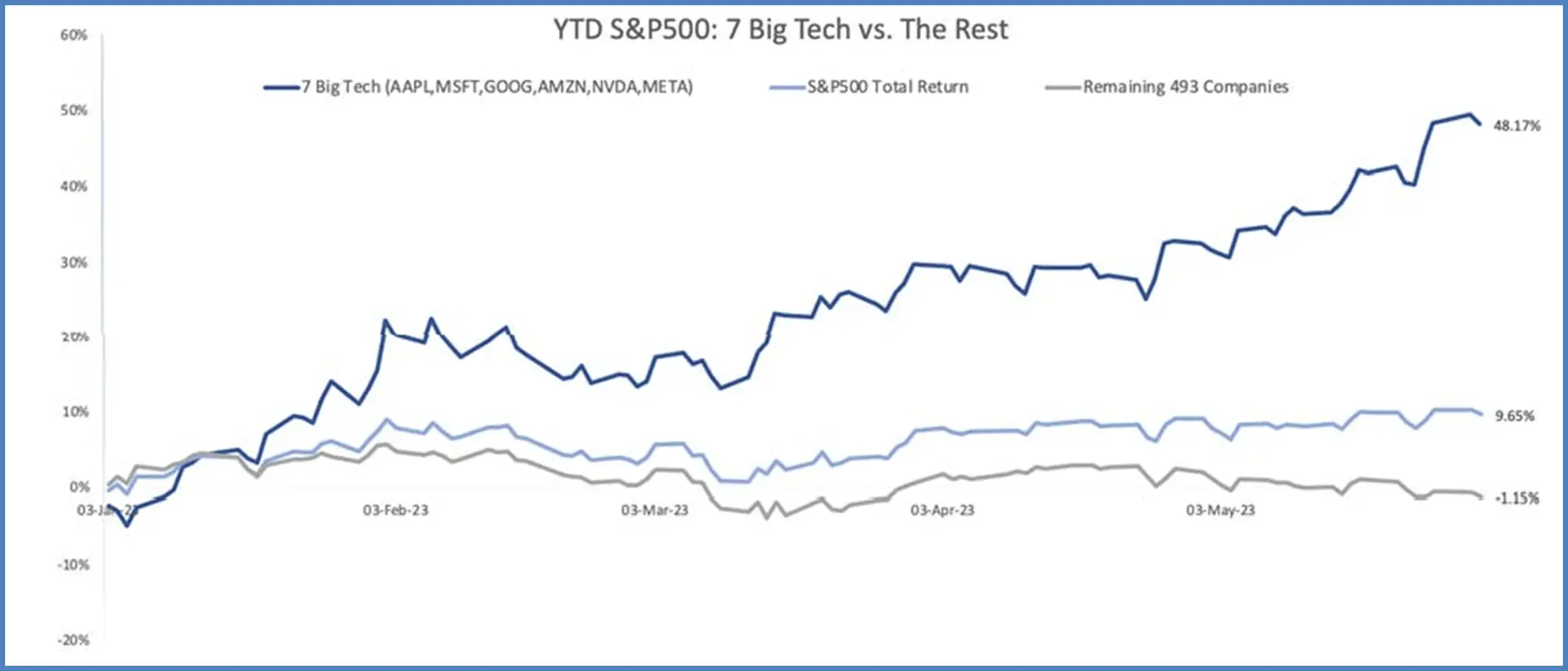

The reality is that generative AI and other new technologies may very well meaningfully improve productivity and create new, successful companies and products and services. However, is there fundamental justification for companies who have been involved in AI for 5+ years to have had their market values increase 35‐170% just this year (Exhibit 1)? At Evans, we do not claim to know which of the hundreds of companies will be most affected by AI. As a result, we refuse to be engulfed by the mania, but instead will continue to buy strong and growing companies with defensible business advantages that are adaptable to their changing environments.

Just as the prospectors enthusiastically descended on California 175 years ago, the exuberance of today’s stock market participants has created overcrowding in a handful of companies. Specifically, large capitalization technology companies continue to outperform the rest of the U.S. stock market significantly and drive the overall index higher (Exhibit 2). Interestingly, this has meant that large parts of the market are relatively inexpensive.

Currently, Apple and Microsoft together account for about 15% of the entire S&P 500. The huge bloat of large cap tech means the S&P 500 is no longer well diversified, being heavily weighted to a handful of companies that are expensive. Both Apple and Microsoft are trading at elevated levels compared to what they were when they were growing faster than they are today. Given their already extreme market penetration and size, it seems hard to believe either company will be able to grow faster than they historically have, but they are priced to do exactly that. From 2010‐2019.

Apple traded at an average price/next‐12‐months earnings ratio (NTM P/E) of 16 times and grew revenue by approximately 16% compounded annually. Today, Apple trades at an NTM P/E of 30 times and is expected to grow revenue only 5% annually for the next three years.

Following the flood of prospectors to California in 1848, two men named Henry Comstock and Ethan Allen Grosh decided to look where the masses weren’t – in Nevada. There they discovered a “holy grail” deposit of gold and silver, more valuable than the site in California. Much like Comstock and Grosh, we believe the best opportunities to outperform will be found where the masses aren’t. As such, we will continue to turn over stones to find great companies at reasonable prices.

WHERE WE’VE TURNED OVER STONES

An example of a good company at a great price we discovered and have been buying recently is Stellantis NV.1 Stellantis is the fourth‐largest automaker in the world by volume, producing approximately six million cars and trucks annually. Its brands include Peugeot, Fiat, Chrysler, Jeep, Dodge, Ram, Citroën, Opel, Vauxhall, Alfa Romeo, and Maserati. The company was renamed Stellantis after the merger of Fiat Chrysler Automobiles (FCA) and Groupe PSA (Peugeot).

The history of Stellantis began with Fiat and its scrappy management team led by the Italian‐ Canadian businessman Sergio Marchionne. Sergio and his team rescued Chrysler Corporation from bankruptcy in 2009, saving more than 300,000 jobs across the industry. After modernizing and investing in the Chrysler, Jeep, and Dodge brands, the company experienced a renaissance in the following years, driving record sales, profitability, and customer satisfaction. This restored both its balance sheet and its standing in the industry, and led to new opportunities including the merger with Peugeot in 2019.

Today, the market capitalization of Stellantis is US$54 billion. The company finished their fiscal year with nearly US$28 billion in net cash (industrial) and firm‐wide profits of US$11.7 billion in 2022. The stock is trading at a mere 2.2 times trailing earnings excluding the net cash in the automotive arm. 2022 was a very strong year for car sales and pricing, although we are skeptical these boom times will persist. We see the company earning US$8 billion annually on a normalized basis, but the business is still exceptionally cheap, trading at less than 6.8x normalized earnings – or 3.3x if you exclude the net cash. The stock currently has a dividend yield of 9% and we are encouraged by the announcement that the company will be buying back 5% of its shares this year.

The naysayers will likely say that the internal combustion engine is dying and that traditional automakers are becoming obsolete. However, management sees its business outlook very differently. It has a goal to double revenues by 2030, while maintaining double‐digit margins, cutting carbon emissions by 50%, and achieving a product mix of 100% electric vehicles in Europe and 50% electric vehicles in North America. We believe Stellantis presents an attractive risk/return: it is priced for obsolescence, but there is a strong likelihood it will still be around and even stronger in the coming decade.

*Some clients might not hold Stellantis NV due to asset mix or timing.

A TIME FOR MORE BONDS?

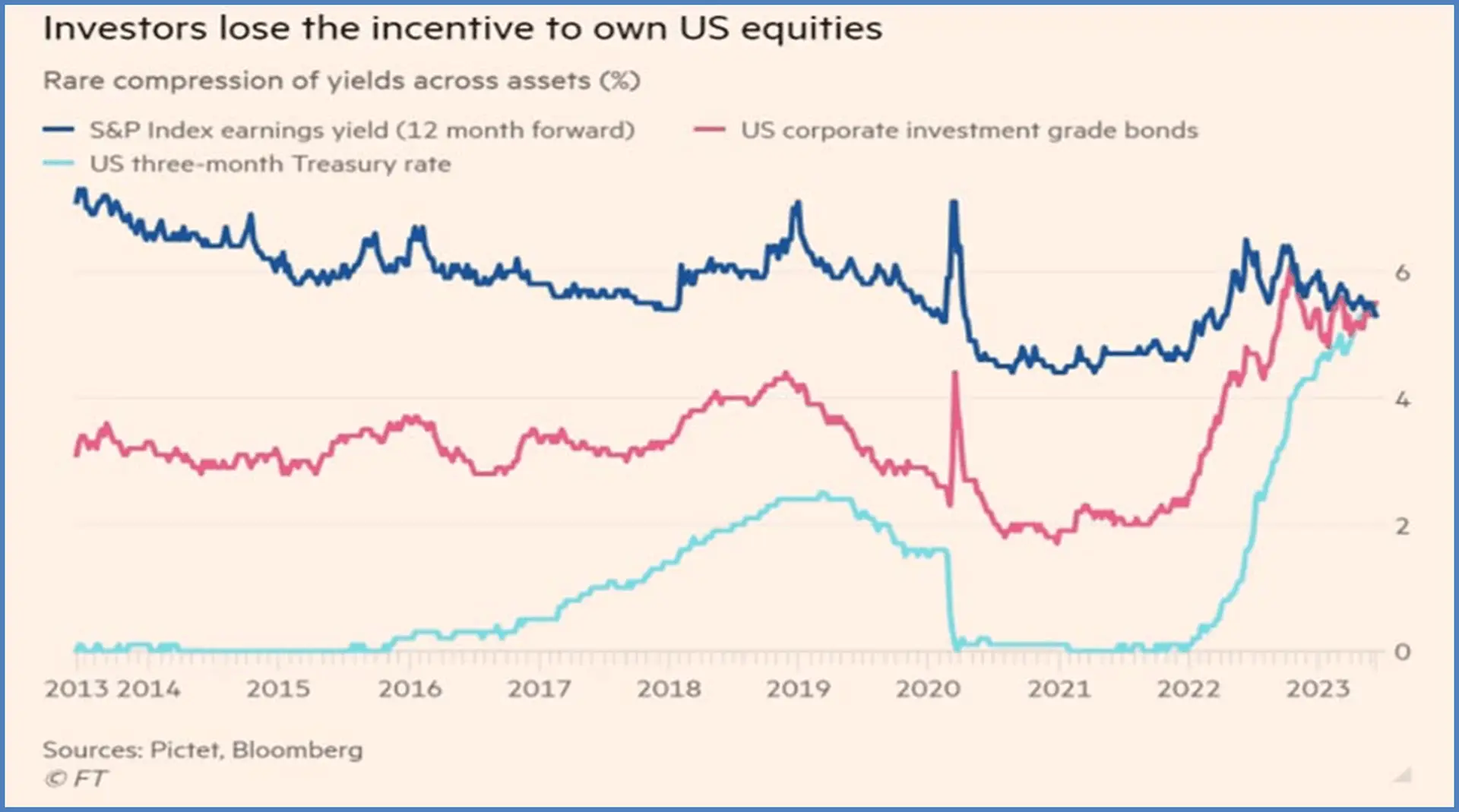

The chart below compares yields of short‐term U.S. treasuries and corporate bonds against the S&P 500 Index equity earnings yield (earnings divided by price). As central banks continue to raise interest rates, the yield on short‐term bonds is now comparable to asset classes with more risk. This begs the question: is it time to allocate more money to bonds?

We have talked before about what drives bond prices, but it’s worth repeating. Key factors to consider include inflation expectations, credit risk, and duration (how long before the bond has to be repaid). Typically, the higher these factors, the higher the rates and the lower the bond price.

While inflation has moderated from its peak, leading inflation indicators have been unexpectedly robust. These include a tight labour market and a healthy U.S. consumer. Even areas highly sensitive to interest rates, such as real estate, have remained resilient. This has led to further interest rate hikes and lower bond prices. Equities, on the other hand, have done well as they provide a better inflation hedge and benefit from the strong economy.

While inflation has been persistent, it is likely that short‐term rates are approaching peak levels as pressure on demand continues to build. Rate increases typically act on a lag of 6‐18 months, which means the demand‐dampening effect is still working its way through the economy. Further, demand has been supported by the pandemic‐driven savings glut, which has now been largely spent.

All this points to a more compelling reason to own bonds than investors have had in several years. We continue to recommend holding shorter duration bonds, which offer higher rates – and lower risk, if the Bank of Canada continues to raise rates.

As we’ve done for the past 35 years, we continue to focus on understanding your needs and providing great value. Our portfolios today hold more profitable, faster‐growing, less levered, and less expensive companies compared to the market as a whole. We will continue to use our resources to turn over stones and uncover great investment opportunities that we expect will benefit you over the long term.

Thank you for your continued confidence and support.

The Evans Team