| Index | Q3 2021 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 0.2% | 17.5% |

| S&P 500 (US$) | 0.6% | 15.9% |

| S&P 500 (C$) | 3.4% | 16.0% |

| MSCI EAFE (US$) | ‐0.4% | 8.4% |

| MSCI EAFE (C$) | 2.3% | 8.4% |

| FTSE TMX Universe Bond Index (C$) | ‐0.5% | ‐3.9% |

| C$ / US$ | 1.2394 to 1.2741 (‐2.7%) | 1.2732 to 1.2741 (‐0.1%) |

* Index returns are total returns, including dividends.

RECAP OF THE QUARTER

The strong market rally of 2021 took a breather in the third quarter. All major stock indices ended Q3 relatively flat after a blistering first half of the year that took them to record highs, and price‐ to‐earnings multiples contracted for the first time in 2021 due to flat prices and improving profitability for companies as they emerge from the worst of the COVID‐19 pandemic.

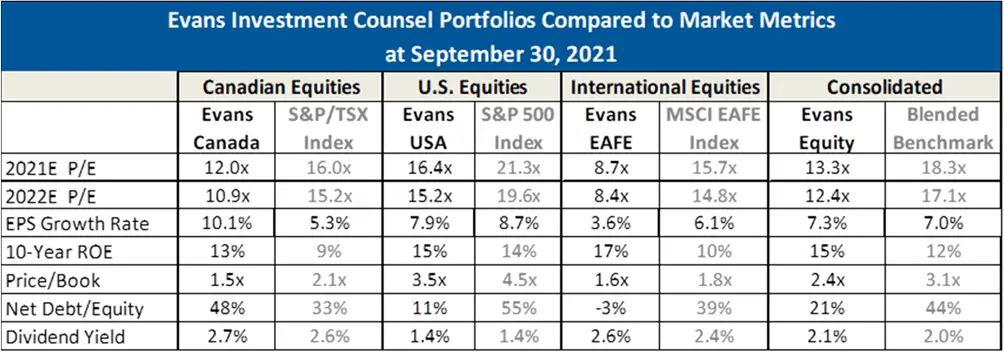

Our blended benchmark currently trades at 18x this year’s expected earnings, compared to 19x at the end of the second quarter, and earnings multiples for our equity holdings now stand at 13x compared to 14x in the previous quarter. Not only are our equity holdings generally less expensive than that of the broader market, they are also more profitable as measured by return on equity (ROE) and are significantly less leveraged as measured by net debt to equity. Additionally, our stock holdings are expected to grow their aggregate earnings faster over the short and medium term, a first since we began tracking these metrics.

Opportunities in the fixed income market remain sparse. New issuances have dropped substantially after a period of rampant refinancing as corporations raised capital at some of the lowest rates ever witnessed. Together with government bond yields rising modestly in the last several weeks, corporate bond spreads have declined to historically low levels, particular for those issues rated investment‐grade.

Bonds deemed “investment‐grade” or “high‐quality” are often perceived to be very safe due to the low credit risk of their issuers. But these bonds still take on interest rate risk and stand to face material losses if rates move up even modestly. This interest rate risk grows more pronounced the longer a bond’s maturity.

Bond prices are inversely related to interest rates: if rates go up, prices go down, and vice versa. For example, prices for Government of Canada bonds maturing in 2051 have fallen by nearly 30% from their peak in March of last year even as yields on the 30‐year bonds rose by just 1.3%. With rates still near historically low levels, and thus prices so high, we remain reluctant to deploy capital and lock in low returns over long maturities, particularly considering recently published high inflation rates. Where we are unable to purchase fixed income investments at returns that we deem acceptable, we are comfortable holding onto cash as we wait for better future opportunities.

GOING AGAINST THE TIDE

In past letters, we mentioned that we own shares of Softbank Group, a Japanese conglomerate whose shares often trade at a substantial discount to the sum of the value of its holdings. A significant portion of Softbank’s value is attributed to its 25% ownership stake in Alibaba Group, one of China’s largest technology companies.

In recent months, Alibaba has found itself at the centre of a broad crackdown by China’s government on an array of different sectors of the country’s economy. Many of these measures have been designed to address long‐running domestic issues in China, but have still been received in a highly negative way by investors in the west, leading to sharp declines in the stock prices of many Chinese companies.

As the negative sentiment deepened, we began buying shares of Alibaba1 directly. We believe that while regulation is likely to dampen the short‐term profitability of many Chinese companies, including Alibaba, it may well over the long term strengthen and clarify the regulatory framework of a country that formerly had none. Furthermore, we believe that the actions taken have not weakened the enduring competitive advantages across Alibaba’s multitude of industry‐leading businesses; in some cases, they have likely even fortified them.

Alibaba is the largest and most dominant e‐commerce company in China, the fastest‐growing consumer economy in the world. A full 20% of all retail sales in China takes place on Alibaba’s platforms; to put that in perspective, Amazon, the largest e‐commerce company in the western hemisphere, accounts for 9% of all retail sales in the U.S. However, Alibaba’s business model is more akin to Google’s than Amazon’s: the company primarily earns its money from fees and commissions paid by merchants and advertisers who seek to sell and market products and services on their platforms. As such, Alibaba’s e‐commerce business operates with a very capital‐light business model and earns exceptional margins and returns on tangible capital that rival some of the very best businesses in the west.

Over the years, Alibaba has used the cash generated by its highly profitable e‐commerce business to build and foster a diverse array of businesses that have become the most dominant in their respective sectors. Chief among these is AliCloud, China’s largest cloud computing platform with over 40% market share, which will likely fare well under the Chinese government’s increased internet security regulation. AliCloud recently became profitable and continues to grow revenues at over 50% a year in a country where cloud adoption is still in its infancy.

Another business is Ant Financial, China’s largest consumer finance and fintech company, in which Alibaba has a one‐third stake. Ant’s planned IPO was halted by government authorities last fall but is still one of the most powerful and valuable fintech companies in the world. Ant owns the ubiquitous Chinese payment app Alipay, which has over a billion users and is the central platform from which the company offers a wide array of different financial services, including deposit‐ taking, consumer and small business lending, investment management and insurance.

Since its IPO in 2014, Alibaba has grown its revenues by nearly 10 times and increased pre‐tax earnings nearly five‐fold. Despite huge investment outlays this year, Alibaba is expected to earn a record US$9 per American Depositary Receipt (ADR), which translates to an earnings yield of 6% on its current market capitalization. Because of its low capital intensity, much of Alibaba’s earnings readily convert into free cash, adding to its burgeoning US$113 billion cash pile, which now accounts for more than a quarter of the company’s entire market capitalization.

If Alibaba continues to invest heavily in its market‐leading businesses even as China’s economy continues to expand, we expect it to continue to be one of the fastest‐growing and most profitable companies in the world. Meanwhile, the company’s stock currently trades at the lowest price‐to‐earnings multiple in its history and ranks nearly the cheapest compared to its competitors.

CONCLUDING THOUGHTS

We have always believed that our ability and willingness to seek investment opportunities wherever they may be gives us an advantage over investors that narrowly focus on a specific region or industry. We have also long stated that our focus on business fundamentals and the long term rather than prevailing popular opinion in the short term enables us to think more rationally in a hyper‐stimulated market dominated by the pursuit of quick profit.

We believe that our approach and adherence to these investment principles have led to a strong track record of performance over the years. But this record has by no means travelled in a straight line. Many of you will remember times where speculation ruled and our style became deeply unpopular, and many of you will also recall periods of severe market panic that saw quick and jarring dips in the market value of your portfolio.

Remaining steadfast during such periods requires a strong degree of trust and belief from you in our approach and process. It is this trust and belief that ultimately enables us to think and act according to our investment principles. For this, we are highly grateful.

Thank you for your continued confidence and support.

The Evans Team