|

Index

|

Q1 2025

|

YTD

|

|---|---|---|

|

S&P/TSX Composite (C$)

|

6.3%

|

31.7%

|

|

S&P 500 (US$)

|

2.7%

|

17.9%

|

|

S&P 500 (C$)

|

1.1%

|

12.3%

|

|

MSCI EAFE (US$)

|

4.9%

|

31.2%

|

|

MSCI EAFE (C$)

|

3.2%

|

25.0%

|

|

FTSE TMX Universe Bond Index (C$)

|

-2.9%

|

2.6%

|

|

C$ / US$

|

1.3921 to 1.3706 (1.6%)

|

1.4389 to 1.3706 (5.0%)

|

* Index returns are total returns, including dividends.

SINGING THE SAME TUNE

At what point does a person get tired of hearing the same story over and over? “Remain patient.” “Valuations matter.” “Discipline is important.” “The S&P 500 is concentrated amongst a few major winners.” Even we sometimes wonder whether repeating these refrains risks making us sound like a broken record, especially in a year like 2025, when growth stocks and anything even loosely associated with artificial intelligence (“AI”) dominated headlines and performance tables. Markets continued to march higher despite geopolitical concerns: Venezuela’s president being captured by U.S. troops; protests in Iran; the continuing conflicts in Ukraine and the Middle East. It can feel pointless to keep singing the same tune while the market seems to be dancing to a very different rhythm.

And yet, history is full of people who repeated an unpopular idea and were eventually proven right. Galileo insisted the Earth revolved around the sun, despite near-universal opposition. Claude Monet painted the same scenes repeatedly, long before the world understood why. Still, for every story of personal vindication, there are countless other people who clung to a belief their entire lives which was never proven correct. Tenacity alone is not always enough.

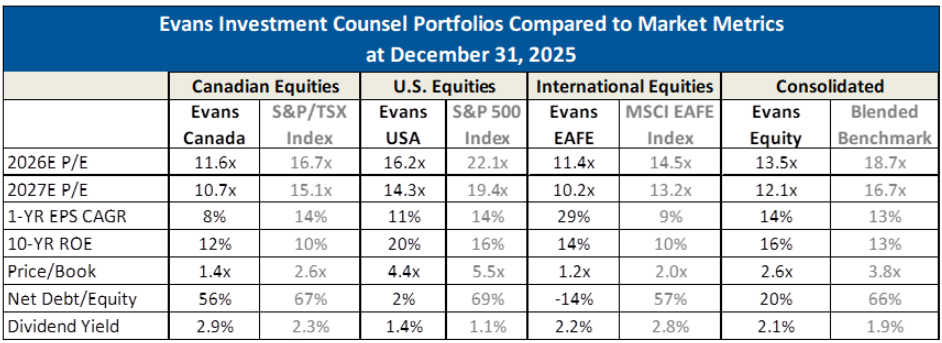

That nuance matters when we talk about “value.” Traditional definitions of value investing may evolve, and yesterday’s metrics may not always fully explain tomorrow’s winners. But some principles remain the same. Paying a reasonable price for a great business with strong economics, reinvestment opportunities, and capable management has consistently been a reliable way to grow wealth over time. That philosophy does not guarantee a win every single year, but it does help investors reach long-term financial goals with fewer unpleasant surprises along the way. The chart below shows how we aim to accomplish this goal for our clients. It compares some key metrics of the companies we hold (under “Evans Equity”) to those of our blended benchmark. Yes, markets may be expensive today, but on average our investments are cheaper (lower price/earnings ratio or “P/E”), more profitable (greater 10-year return on equity, shortened to “ROE”) and less indebted (lower net debt/equity) than our benchmark.

It is also worth noting that while much of the narrative in 2025 focused on U.S. growth stocks and AI-related enthusiasm, the past year delivered a broad diversification of returns. International and Canadian markets outperformed U.S. equities, an outcome that would have seemed hugely unlikely to many just a year ago. It serves as a useful reminder that markets rarely reward the same exposures indefinitely.

So we may indeed be guilty of singing the same tune. But repetition is not stubbornness; rather, it is conviction shaped by experience. Markets change. Themes rotate. Narratives come and go. But holding to the discipline of thoughtful pricing, diversification, and patience has paid off through many cycles. In a year filled with noise and novelty, we believe there is still value in returning to the fundamentals, even if it means listening to a familiar song yet again.

LESSONS FROM A CAREER OF COMPOUNDING

The legendary Warren Buffett recently announced his intention to step back from the day-to-day leadership of Berkshire Hathaway, marking the beginning of the end of one of the most remarkable investing careers in history. When Buffett took control of Berkshire in the mid-1960s, it was a struggling textile business; over the following six decades, it became one of the largest and most successful companies in the world. Long-term shareholders have been rewarded handsomely for their patience, benefiting not from short-term attempts to time the market, but from disciplined decision-making and repeated compounding over time.

Since Buffett assumed control, Berkshire’s share price has increased astronomically, turning modest early investments into generational wealth. While few investors owned Berkshire from the very beginning, the lesson is a good one: exceptional businesses, paired with exceptional capital allocation, can compound returns far beyond what most people believe is possible. Importantly, this success was achieved with remarkably little complexity – no leverage-driven speculation, no quarterly earnings games, and definitely no attempt to predict macroeconomic outcomes.

Berkshire’s structure has been central to this outcome. The company does not pay a dividend, preferring instead to reinvest internally where returns are attractive. It repurchases its own shares when management believes its stock is trading below intrinsic value, increasing each remaining shareholder’s ownership over time. Capital is allocated thoughtfully across wholly-owned businesses, public equities, and cash reserves. Crucially, patience is viewed as a strategic advantage, not a cost.

Berkshire Hathaway serves as a powerful case study in what disciplined ownership can achieve over the long term. It demonstrates that enduring wealth is often built through patience, sound judgment, and a willingness to let compounding do the heavy lifting. As Buffett transitions away from the helm, the legacy he leaves behind is not just a company. It is a philosophy that will continue to shape how we think about long-term investing.

HOLDING YOUR WINNERS

With some of our heavily weighted holdings benefiting meaningfully from the recent wave of enthusiasm around artificial intelligence, and with increasing speculation about a potential “AI bubble”, you may be asking if it is time for us to sell companies like Google and Samsung.1 The answer, as is so often the case in investing, is not that simple.

Strong recent performance alone is rarely sufficient reason to exit a high-quality business. In certain circumstances, continuing to hold a successful investment can still be the right decision, even after a strong period of appreciation. If a business can consistently grow its earnings and strengthen its competitive position, shareholders can continue to benefit by allowing that progress to compound over time. Selling purely because a stock has performed well risks missing out on the very growth that drives long-term returns. In these situations, patience and discipline can be a more reliable source of value than attempting to time entry and exit points precisely.

There is also another practical, often overlooked benefit to long-term ownership: tax efficiency. Holding durable compounders allows capital to remain invested rather than having returns eroded by repeated tax realization. Additionally, companies like Google and Samsung provide exposure to

powerful long-term growth themes such as artificial intelligence and semiconductors at valuations that remain reasonable relative to other companies in this sector. For example, Micron, another semi-conductor manufacturer, trades at a forward-12-month price to book ratio of 5.5x versus Samsung at 2.25x. While Samsung and Google may look expensive on an absolute basis, we believe their quality, earnings power, and strategic positioning continue to justify long-term ownership.

That said, although we still like them as long-term businesses, it is worth noting that we may be trimming our positions, either if they reach or exceed our view of fair value, or if the portfolio weighting in these positions exceeds the concentration level we are comfortable with for clients. There is always a balance to strike as we work to protect and grow clients’ wealth for years to come.

1 Some clients may not hold Google or Samsung due to asset mix or timing.

YEAR IN REVIEW

The firm had an incredible year of growth. We are now managing over $2.4 billion of assets for nearly 400 families, and we continue to add capacity, personnel, and automation to enhance the experience we provide our clients.

In 2025, two new staff members joined our team: Heidi Gu and Matthew Febbraio. Heidi serves as an Operations and Financial Associate, supporting Janelle Li, our Director of Operations, in implementing new systems and firm-wide automation to improve efficiency so we can spend more time on what matters most – helping clients achieve their financial goals and delivering the highest standard of investment management. Matthew joined us as our newest Wealth Associate and Client Relationship Manager. By adding younger team members, we aim to continue growing the firm while maintaining the high level of service our clients have come to expect. Matthew plays an important role in advancing that mission.

We are deeply grateful for the trust our clients place in us as stewards of their hard-earned savings. We remain committed to earning that trust every day through outstanding service and disciplined, prudent investment management. 2025 was an exceptional year, and we look forward to reaching many more milestones together in the years ahead.

Thank you for your continued confidence and support.

The Evans Team