| Index | Q4 2021 | 2021 |

|---|---|---|

| S&P/TSX Composite (C$) | 6.5% | 25.1% |

| S&P 500 (US$) | 11.0% | 28.7% |

| S&P 500 (C$) | 10.5% | 28.2% |

| MSCI EAFE (US$) | 2.7% | 11.3% |

| MSCI EAFE (C$) | 2.3% | 10.8% |

| FTSE TMX Universe Bond Index (C$) | 1.5% | ‐2.5% |

| C$ / US$ | 1.2741 to 1.2678 (+0.5%) | 1.2732 to 1.2678 (+0.4%) |

* Index returns are total returns, including dividends.

RECAPPING THE YEAR

2021 was yet another year that saw surging stock markets. In local currency terms, the S&P 500 and the S&P/TSX Composite returned 29% and 25% respectively. The two indices are now 48% and 24% higher than they were at the end of 2019, before the COVID‐19 pandemic struck, and their underlying earnings have grown at a somewhat slower but still impressive rate of 26% and 21%. In contrast, the EAFE index, containing no U.S. or Canadian stocks, returned in 2021 a much more muted 11% in Canadian dollars, and is just 12% higher over the past two years. Its earnings have remained essentially flat.

The strong earnings growth of North American stocks reflects the incredible resilience of these economies in the face of the significant negative effects of the COVID‐19 pandemic. While many businesses and sectors continue to be hurt badly by the pandemic, others have benefited substantially. In particular, earnings from stocks in the Information Technology sector of the S&P 500 grew enormously, up nearly 50% from 2019.

The pandemic’s varying effect on different areas of the economy is reflected in the skew in returns for the year across the stock market. Additionally, the pockets of speculative fervour that we saw in 2020 intensified in 2021, further driving price momentum for a chosen few stocks that have recently been in vogue. Consider this statistic that illustrates the difference between the haves and the have‐nots: just four of the 500 stocks in the S&P 500 accounted for more than one‐third of the index’s entire return for the year.

That these select few companies were primarily responsible for driving stock indices higher means, of course, that most other stocks experienced far more modest price increases. Indeed, earnings for the average company grew more than their stock price in 2021, leading to a decline in the price‐to‐forward‐earnings multiple of S&P 500 equal‐weighted index despite 2021’s strong market performance.

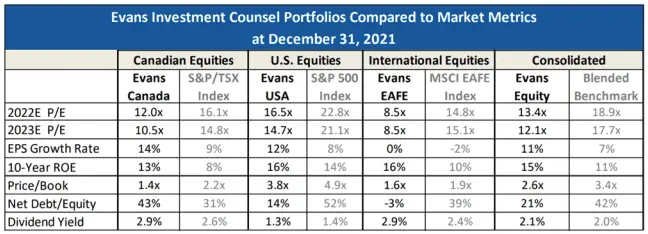

The decline in earnings multiples was true for our stock holdings as well. Overall, our equity holdings currently trade at a price‐to‐forward‐earnings multiple of 13x, down from the 15x where it was trading at the end of 2020. This multiple represents a five‐point discount to our benchmark’s multiple – one of the largest discounts in recent memory. In addition, we anticipate that our companies will generate their highest earnings growth in aggregate that they have in years, as our holdings stand to benefit significantly from a strengthening economy and rising interest rates.

THE “SAFEST” BONDS ARE SOMETIMES THE RISKIEST

2021 was also the year in which many of the world’s central banks began to reduce pandemic‐era monetary stimulus, or at least indicate that they were about to, in the face of rapidly‐rising inflation. This contributed to a sudden rise in rates that in turn spurred steep price declines for bonds with the least credit risk. As mentioned in previous letters, this chain of events might seem counterintuitive but can be attributed to duration risk, which has a large negative impact on the price of long‐maturity bonds that have low yields.

As an example, prices for some long‐maturity U.S. Treasury bonds, the safest of all assets in terms of principal risk, have fallen by close to 20% since they were issued during the onset of the pandemic in the spring of 2020. This illustrates the risk of buying long‐term bonds that pay a mere 1% per annum in interest. Demand for higher yields was also seen in the corporate bond market, where non‐investment grade rated corporate bonds far outperformed their investment grade rated counterparts. The Bloomberg U.S. Corporate High Yield index returned 5% for the year compared to ‐1% for the Bloomberg U.S. Corporate Investment Grade index, a staggering disparity in the bond world where even tenths of a percent matter.

As seen above, even the highest quality assets can yield poor returns if they are priced poorly. Conversely, lower quality assets can yield far better returns than might be originally thought. We have long stated that we are highly reluctant to lock in low returns for long periods, even if the investments are considered risk‐free. With inflation presently many times higher than the rates being offered on the lowest‐yielding and highest‐quality bonds, buying them right now will virtually ensure that purchasing power is eroded over time.

We have always favoured corporate bonds that are of high credit quality but are not perceived as such; they offer far better return prospects than those of issuers whose high credit quality are well known. We have also liked and continue to like preferred shares from high quality issuers that pay yields that fluctuate with the movement of interest rates.

Nonetheless, we continue to have difficulty finding a lot of fixed income securities that meet our requirements for both return and risk. Rather than lowering our investment standards, we will simply wait until a better environment for buying bonds returns. In the meantime, we intend to keep the duration of our fixed income portfolios lower than that of the benchmark to mitigate duration risk and maintain a higher degree of liquidity in our portfolios, so we can take advantage of opportunities when they do arise.

AN ILLUSTRATION OF OUR PROCESS

In late 2020 and early 2021, we started buying shares of Loblaw Companies1, which owns its namesake, Canada’s largest grocer, and Shoppers Drug Mart, the country’s biggest pharmacy chain. With over $53 billion in revenue, Loblaw operates on a scale large enough that it can deliver reasonable prices, and offers convenience through a base of over 2,400 stores located in city centers across the country.

At the time that we bought it, Loblaw was trading at less than 15 times its expected forward earnings, a price that we thought was relatively cheap for a stable, high‐quality business. Loblaw has been a big beneficiary of the pandemic’s effects over the past two years, as restaurants remained closed for extended periods and people stayed at home. Perhaps more importantly, Loblaw is now benefiting from surging inflation in food prices at levels not seen in years. Loblaw’s same‐store sales growth accelerated to nearly 9% in 2020 and the company has been able to maintain these gains in 2021 even as the Canadian economy reopened.

Some investors are doubtful that the huge sales gains will continue as the economy returns to normal, and this concern was reflected in Loblaw’s price at the time of our purchase. While pandemic‐era demand trends will not last forever, higher than normal inflation in the food sector appears likely to stay for the foreseeable future. This is a huge positive for Loblaw, as the company can raise prices quickly, generating strong operating leverage over a largely fixed cost base and thereby significantly enhancing earnings and returns on capital. Loblaw has also made significant strides in improving the efficiency of its operations, such as automating check‐out to reduce overhead costs and waiting times.

Over the course of the year, Loblaw’s stock price rose from less than $70 to above $100, where it stands today. We recently sold Loblaw from client accounts as its price had risen to 18 times its expected earnings for this year, a valuation which we believe is now more in line with our estimate of its intrinsic value compared to when we first began purchasing the stock.

SPECULATIVE EXCESS

The process of analyzing a business and determining its value by estimating what it would likely produce in future earnings and cash flows might feel quaint and old‐fashioned in today’s environment. Over the course of the past year, price momentum drove a handful of stocks to record levels on a seemingly regular basis. At the same time, speculative booms exploded in a wide array of different assets that in some cases have crossed into the absurd. From meme stocks to cryptocurrencies and non‐fungible tokens (NFTs), it seemed like there were an endless number of fashionable new bandwagons on which to hop, if one was so inclined.

At a time like this, we find it useful to repeat to ourselves – and to you – what investing is, at its core: the setting away of money now to have more in the future. We believe that this future bounty can only be reliably determined by what the asset itself actually produces, not by speculation on what a future buyer might be willing to pay for it. We believe that the price of all things will ultimately come to reflect that philosophy.

We do not do things solely because others are doing so, nor do we choose investments in the hopes of turning a quick profit. That is not a game that we play or ever have played, although we do not begrudge those who do. Instead, we stay disciplined in our investment philosophy and focused on our process of finding quality businesses that are selling at attractive prices. We invest our own money alongside that of our clients, and always remain mindful that most of you have entrusted a substantial portion of your wealth with us.

Thank you for your continued confidence and support. All the best to you for 2022.

The Evans Team