| Index | Q4 2022 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 6.0% | ‐5.8% |

| S&P 500 (US$) | 7.6% | ‐18.1% |

| S&P 500 (C$) | 6.4% | ‐12.4% |

| MSCI EAFE (US$) | 17.3% | ‐14.5% |

| MSCI EAFE (C$) | 16.1% | ‐8.5% |

| FTSE TMX Universe Bond Index (C$) | 0.1% | ‐11.7% |

| C$ / US$ | 1.3707 to 1.3557 (1.1%) | 1.2678 to 1.3557 (‐6.5%) |

* Index returns are total returns, including dividends

2022: A RETURN PROFILE NOT SEEN FOR HALF A CENTURY

“History doesn’t repeat itself, but it often rhymes.” – Mark Twain

With 2022 now in the rearview mirror, we reflect on a year in which stocks and bonds finished significantly down. Investors have not seen a year with negative returns for both major asset classes in over fifty years, when rapid inflation in the mid‐1960s forced the Federal Reserve to increase interest rates. The result was that in 1969 the economy tipped into a recession, and bonds and stocks both showed negative returns.

This past year central banks responded aggressively to runaway inflation by raising interest rates from 0.25% at the start of the year to a much more restrictive 4.25% by year‐end. Interest rates act as a gravitational force on all assets: the more the force of gravity increases and interest rates rise, the faster we are pulled down to Earth when asset prices fall. As a result of the sizeable interest rate hikes last year, both stock and bond prices reset lower to reflect the new opportunity cost in this higher interest rate environment. This downturn is in noteworthy contrast to more recent bear markets like the technology bubble, great financial recession and the COVID pandemic, where bonds increased as stocks fell. Those past downturns were characterized by the movement of capital from riskier assets to safer ones, rather than an overall reset of investors’ opportunity cost caused by central banks increasing the “risk‐free rate”, the theoretical rate of return on an investment with zero risk.

2022 saw the S&P 500 decline 18.1% (US$), its worst year since 2008, when it was down 37.0% (US$). The Nasdaq Composite, heavily weighted with technology stocks, fared even more poorly, falling 32.5% (US$). The S&P/TSX performed better than its U.S. counterparts, down only 5.8%, buoyed by the strong performance of the energy sector (representing 18% of the total index) which itself was up 30.3%. In contrast, the S&P 500 did not benefit nearly as much from its energy sector, which was up 59%, as it only represented 2.7% of the total index. The Canadian bond market posted a negative return, its first bear market in almost 40 years, with the FTSE Canada Universal Bond Index down 11.7%. Lastly, cryptocurrencies joined the misery with bitcoin starting the year at US$46,334 but finishing it at US$16,540, a tumble of 64%. The massive declines seen in the heavily technology weighted NASDAQ Composite and especially in cryptocurrencies reinforces our philosophy at Evans to preserve and grow wealth by avoiding fads, instead investing in strong, profitable companies with significant competitive advantages at reasonable prices.

WHO LET THE INFLATION OUT?

“Inflation swindles the bond investor, it swindles the person who keeps their cash under their mattress, it swindles almost everybody.” – Warren Buffett

Inflation hit us all in 2022, whether filling up our tanks at the gas station or buying the very basics at our local grocery store. This year we saw inflation peak in Canada at 8.1% year over year, the fastest annual increase since 1983, and 9.1% year over year in the United States, the quickest pace on record since 1981.

A perfect storm led to the dramatic change in consumer prices in 2022. The primary driver of inflation in recent years has been the record levels of monetary and fiscal stimulus injected into the economy following the COVID‐19 outbreak. In 2020 and 2021 monetary stimulus in the U.S. totaled $4.4 trillion, or 18% of 2021 GDP, and fiscal stimulus totaled $5 trillion, or 21% of 2021 GDP. The level of stimulus following the pandemic was unprecedented, and as the CEO of JP Morgan, Jamie Dimon, mentioned in his annual letter, this stimulus was and will always be inflationary.

In February the global markets faced a significant supply shock from the response to the war in Ukraine. NATO forces banded together to boycott Russia, reducing the supply of many important commodities including metals, hydrocarbons, and agricultural goods.

The uneven reopening of world economies in the aftermath of COVID also contributed to inflation this year. China’s zero COVID policy was in sharp contrast to the rest of the world’s approach; this had a pronounced impact on most supply chains. Governments responded to these developments with an increased effort to move foreign production back domestically. This in turn led to price increases because of the differences in labour costs between developed and developing countries, and these costs were often passed on to the consumer. This partial reversal of globalization marked a significant departure from the disinflation we had enjoyed over the last 20+ years.

A shortage of labour in North America contributed to inflation as well, as it continued to put upward pressure on labour costs. Companies have recently been aggressively competing for talent, offering higher salaries to attract and retain key employees. The companies who are able to do so have passed on the higher labour costs by raising the prices of their goods. While immigration is helping this situation in North America, participation in the labour force continues to remain below pre‐pandemic levels.

In the fight to tame inflation, the Bank of Canada and the U.S. Federal Reserve both began tightening monetary policy in March by increasing short‐term interest rates. Last year, both central banks increased interest rates seven times in their efforts to bring inflation back to their ultimate target of 2%. How many more rate increases the central banks will make is unknown. Tightening too much could lead to a deep recession, while tightening too little could lead to inflation getting out of hand.

At Evans we frequently discuss the economic outlook and how it will affect the companies we own. However, we believe trying to predict the Fed’s next hike or get the next read on inflation is a futile endeavor. Instead, we continue to focus on understanding the individual businesses we own and look to invest in companies that can survive and take advantage of the opportunities that a tough macroeconomic environment provides. This strategy has served our clients well over the firm’s 30‐year history.

SAVERS ARE BEING REWARDED AGAIN

North American bond yields have risen to compensate for inflation and the central banks’ rate increases. Shorter‐term bond yields have increased more than longer‐term yields, suggesting that the bond market believes that central banks will be successful in taming inflation in the shorter term, i.e., in less than five years. This can be seen in the chart below of the yield curve for the Government of Canada bond yields as of December 30, 2022 (green line) compared to yields from December 31, 2021 (purple line), showing bond yields for maturities spanning three months to 30 years.

Yields for all maturities increased in 2022, but especially for shorter‐term maturities. For example, the yield for three‐month T‐bills increased by more than four percentage points (from 0.17% to 4.24%), whereas the yield for the Canada 30‐year bond only moved up by 1.6 percentage points (from 1.7% to 3.3%). Due to the uneven shifts in bond yields, the yield curve in 2022 became “inverted”, meaning that short‐term rates were higher than long‐term ones. When government bond yield curves become inverted, a recession is likely to occur within approximately the next twelve months. When inflation does finally abate, short‐term yields should fall below long‐term yields and return the yield curve to an upward sloping shape like the one in the chart for December 31, 2021.

Bond yields and prices are inversely related – when yields fall, prices rise, and when yields rise, prices fall. Since most bonds have fixed interest rates, and their coupon payments do not change over the life of the bond, the only way for bond yields to adjust to the prevailing interest rate environment is for the bond prices themselves to change – down for an increase in yield, or up for a decrease.

Our bond portfolio fared better than the bond benchmark last year due to having a lower duration (4.2 years vs. the benchmark’s 7.4 years). We believe that when inflation returns to a level the central banks are more comfortable with, short‐term rates and yields should fall more than those with longer maturities. This would benefit many of our bond holdings.

WHERE WE FIND INEFFICIENCY IN THE BOND MARKET

At present, we believe that government bonds, with their low return profile, do not make great financial sense. In addition, many investment grade corporate bonds do not provide an adequate yield when compared with many non‐investment grade bonds. Listed below are highlights of a few bonds we hold, issued by Morguard Corporation and Russel Metals, which we believe offer higher yields in exchange for misunderstood credit risk profiles by the market.

We hold the following Morguard bonds:

| Coupon | Maturity | Yield‐to‐Maturity | Duration |

|---|---|---|---|

| 4.40% | 28‐Sept‐2023 | 7.8% | 0.7 years |

| 4.71% | 25‐Jan‐2024 | 7.9% | 1.0 years |

| 4.20% | 27‐Nov‐2024 | 7.6% | 1.8 years |

Morguard is a real estate investment company whose principal business activities include the acquisition, development and ownership of multi‐suite residential, commercial and hotel properties. Morguard is also a real estate investment advisor and management company, representing major institutional and private investors. Morguard’s total assets under management (including both owned and managed assets) were valued at $19.5 billion as of September 30, 2022.

Like most real estate companies, Morguard is leveraged, but it has decent assets to back its debt and a strong tenant base. Also, the company generates revenue from several sources: its management and advisory services platform; corporately owned assets; and the distributions received from its investments in Morguard REIT and Morguard Residential REIT.

Our holdings of Russel Metals’ bonds are of the following two issues:

| Coupon | Maturity | Yield‐to‐Maturity | Duration |

|---|---|---|---|

| 5.75% | 27‐Oct‐2025 | 6.5% | 2.5 years |

| 6.00% | 16‐Mar‐2026 | 6.7% | 2.8 years |

Russel Metals is one of the largest metal distributors in North America. With nearly 70 metals service centres in Canada and the US, Russel Metals’ primary business is processing and distributing pipe and stainless steel and aluminum tubular products, as well as carbon hot rolled and cold finished steel, to the construction and equipment manufacturing industries. Russel Metals’ energy tubular products unit distributes flanges, tubes, valves, and fittings to the energy industry. The company also distributes steel products (plates, beams, and pipes) for large volume sales to steel mills and other distributors. About 65% of Russel Metals’ sales come from Canada.

The company has a strong balance sheet and benefits from scale and strong market positions in Canada and the U.S. South and Midwest regions. We believe these outweigh the risks of the cyclical nature of the steel and metals industry and their transactional business model that does not have long‐term customer contracts. Despite its strong balance sheet, the company has been given a below investment‐grade credit rating of BB+ by S&P, largely because of the company’s small size. This ‘high yield’ or ‘junk’ rating provides us with an opportunity to purchase these bonds at a discounted price: most institutional investors are not allowed to buy high yield bonds, which substantially reduces the demand for these bonds.

Russel Metals’ management is highly capable and has done a commendable job managing inventories through both good times and bad. The company’s cash flows are counter‐cyclical due to the timing of inventory purchases. When times are good, Russel Metals increases its inventory of metals to meet higher demand. During slower periods when sales are lower, the company reduces inventory levels by not replenishing them as quickly, freeing up cash to support the business.

CONTINUING TO FIND VALUE IN THIS MARKET

Onex Corporation (ONEX:TO)1 is a Toronto‐based asset management firm that was founded in 1984 by Gerry Schwartz. Schwartz started the company after a brief stint at Bear Sterns, where he learned about the leveraged buyout model and famously worked with Jerome Kohlberg, Henry Kravis and George Roberts, who subsequently left Bear Sterns to start KKR & Co. together.

Having followed Onex over the years, we have watched it grow from a small private equity company into a much broader, full‐service financial platform. The journey began in 2007 with Onex diversifying into private credit, which was later bolstered by their acquisition of Falcon Investment Advisors in 2020. In 2019, the acquisition of Gluskin Sheff brought them into the realm of public equity and credit. Since then, they have further expanded their services to offer wealth and estate planning. We believe they have an attractive platform to service the financial needs of institutions, high net worth families and endowments.

Over the last 25 years, they have an excellent track record: Onex has grown shareholders’ capital from US$740 million in 1997 to US$7.6 billion in the most recent quarter, a more than tenfold increase before taking into consideration share repurchases and dividends paid. Their repurchase program has returned US$2.8 billion to shareholders over this period and reduced the shares outstanding by nearly 60%.

The valuation discount today is the most extreme it has been since the financial crisis of 2008‐2009. Shares in Onex traded for C$65.29 at year end, which is nearly a 48% discount to the reported value of their investments of C$123.71 per share. We think the stock offers an attractive risk/return profile today and our confidence in the company is further boosted knowing that its own management continues to repurchase shares aggressively at these prices.

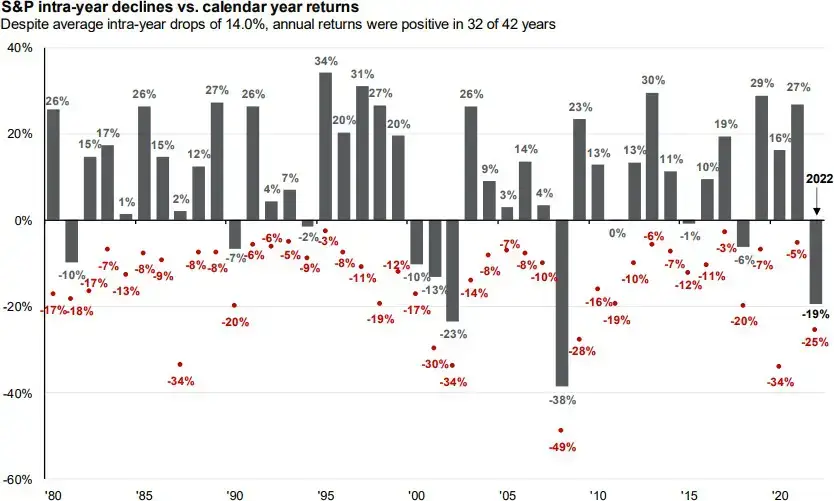

STAY THE COURSE

When sailing through a storm, changing winds and crashing waves can create panic among passengers. It’s the crew’s job to stay the course and navigate safely and successfully. Our team follows the same principles. As shown below, the market has dropped over 10% at some point intra‐year 22 times. But, like the crew of a ship, we remain steadfast in our approach during turbulent times, don’t panic, and continue to invest using the same philosophy we always have. For over 30 years our team has remained calm in the face of uncertainty and taken advantage of others’ panic by buying into great companies at cheap prices. This has led to a strong long‐term track record.

Thank you for your continued confidence and support.

The Evans Team