| Index | Q1 2019 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 13.3% | 13.3% |

| S&P 500 (US$) | 13.7% | 13.7% |

| S&P 500 (C$) | 11.3% | 11.3% |

| MSCI EAFE (US$) | 10.0% | 10.0% |

| MSCI EAFE (C$) | 7.7% | 7.7% |

| FTSE TMX Universe Bond Index (C$) | 3.9% | 3.9% |

| C$ / US$ | 1.3642 to 1.3363 (+2.1%) | 1.3642 to 1.3363(+2.1%) |

* Index returns are total returns, including dividends.

PRICE VERSUS VALUE

What a difference three months can make! The first quarter of 2019 saw a near reversal of the significant price drops experienced by major equity indices during the last few months of 2018. Just as the S&P 500 posted its worst loss for a fourth quarter since 2008, it recorded its highest ever first quarter gain in well over a decade. The gain of the index was just short of its all‐time high level reached in mid‐2018.

The near 180‐degree turn in just three short months reveals the futility of trying to predict market prices. In the midst of the market downturn last year, the business news media was riddled with gloomy predictions of continued and prolonged market declines. Even though these forecasts have not transpired, history has shown that repeatedly wrong predictions have not discouraged market prognosticators from continuing to do so nor has it shrunk their audience. In our view, no one can accurately predict the direction of market prices. But neither do we need to – we simply seek to use fluctuations in prices to purchase companies that we like at lower prices and to trim or sell holdings as their prices approach or exceed their intrinsic values.

Price and value are often conflated with each other, but the two could not be more different. Put simply, price is what you pay and value is what you get. A company’s intrinsic value reflects the future earnings stream accruing to its owner and changes little on a daily basis. During periods of heightened market volatility, like that of late 2018, ownership interests in companies were regularly changing hands at prices that vary four to five percent each day.

For example, BorgWarner Inc.1, a company that we own, whose stock price dropped from $54 in April 2018 to a two‐year low of $33 on Christmas Eve and has since climbed back to $42. The fact that BorgWarner, a leader in its industry, can be valued at 40% less than they were just eight months prior makes no sense to us. But, that was what the market was offering for BorgWarner’s shares.

To us, the value of BorgWarner changed little between April and December of 2018, but the 40% off sale on its stock gave us an opportunity to purchase a great business at a far better price. Such a proposition should seem obvious but investors often approach buying and selling stocks in the exact opposite fashion that they approach buying and selling everything else. They frequently get in their own way, vacillating between greed and fear as markets rise and fall. In missing the distinction between price and value, they forget that the market is there to serve us, and not the other way around.

SNC‐LAVALIN

SNC‐Lavalin is the largest engineering and construction company in Canada, employing over 50,000 employees in 50 countries and generating over $10 billion in revenues last year. It also owns investments in infrastructure concessions, where the vast majority of its value is a 17% stake in the 407 Express Toll Route (ETR), a toll‐taking highway stretching east‐west just north of Toronto. When we started purchasing shares of SNC2, we estimated that the 407 ETR was worth in the ballpark of $27 per share, leaving a very moderate price paid for the company’s engineering and construction businesses.

This discount was in large part due to a bribery scandal going back to 2001 that ultimately led to the firing of all previous senior management. SNC had sought, and was later denied, a deferred prosecution agreement (DPA), which is a provision allowing companies and the employees untarnished by past misdeeds to operate without the shroud of a criminal trial. The refusal was surprising as SNC’s new management fired all the individuals responsible and made significant remediation efforts in changing the company’s culture and implementing a world‐class ethics and compliance framework. DPAs are also common throughout the world and, ironically, some of SNC’s peers are now competing with the company while operating with a DPA.

Earlier this year, the company became ensnared in a full‐blown political scandal when Canada’s former attorney general made public her belief that the Prime Minister’s Office had tried to influence her to secure a DPA in the company’s favour. This revelation has greatly complicated any possibility of a rational compromise for the company in the near‐term as politics has taken center stage in the situation, resulting in all three political parties jostling for favourable positioning during a federal election year.

All of this has understandably created a giant cloud of uncertainty over SNC, pushing its stock to lows not seen since the worst of the Great Recession. Even though we are unhappy with the developments of the company, we believe that its stock price has been pushed to a level that now gives little credit to its fundamental value.

In contrast to the attention it’s been given by our national media, Canadian federal contracts are now a small part of SNC’s business, with only one remaining in its backlog. And even in the absence of a DPA, the company can still bid on provincial contracts, where the lion’s share of the country’s infrastructure spending takes place. Moreover, a recently announced sale of a portion of the 407 ETR will leave the company with a significantly less levered balance sheet, allowing for new options to deploy capital, including share repurchases. Lastly, SNC’s engineering consulting business, built through its 2017 acquisition of UK‐based Atkins, now accounts for over 70% of its total engineering and construction operating earnings. These factors in combination yield a value well north of what the company’s stock is selling for.

MANAGING EXPECTATIONS

The events that have transpired at SNC continue to remind us of the inherently uncertain environment that we operate in, where anything can happen. By definition, it isn’t the possibilities that we are aware of and spend most of our thinking about that catch us off guard, but the ones that seem most remote. As investors, we must be constantly cognizant of this fact, appropriately building in sufficient margins of safety when we buy shares of companies. With all else equal, margins of safety enlarge as prices fall and narrow as they rise.

As equity prices have jumped sharply at the beginning of the year, investors in general have once again become more optimistic about returns. The rise in prices virtually ensures that future returns will be lower than they were when equities almost reached a bear market last year. It’s not just equity returns that will likely be lower; investors should expect lower returns across all asset classes. In an environment where the 10‐year U.S. Treasury bond yields just 2.5% and the 10‐year Bank of Canada bond yields 1.7%, prospective returns will likely be a lot lower compared to the returns that we have seen over the last 10 years.

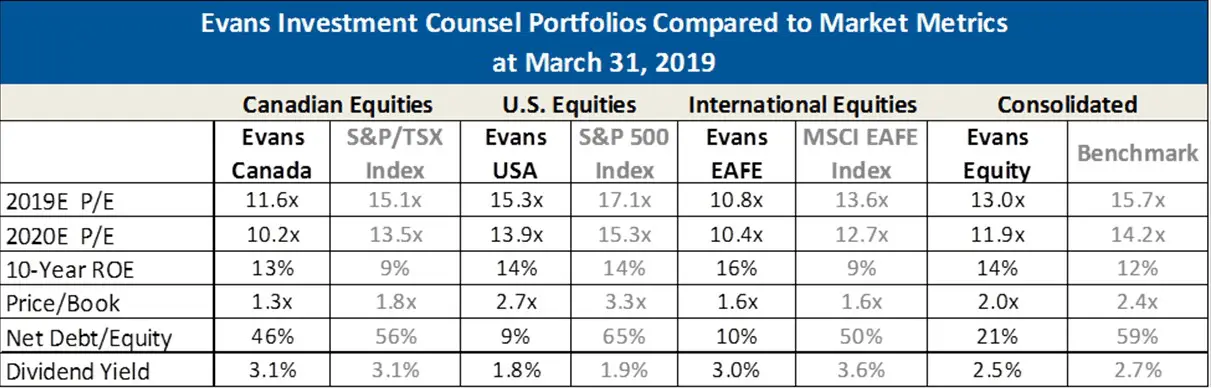

Nonetheless, we believe that carefully selected companies purchased at reasonable prices continue to present the best investment option. We believe that our overall portfolio comprises of companies that are more profitable as measured by 10‐year average return on equity (ROE) and less financially levered when comparing net debt/equity ratios. And finally, the companies that we own are also less expensive as a whole based on price‐to‐earnings multiples.

In a naturally uncertain world, we are only sure about a few things: negative events will inevitably effect some of the companies that we own and we will make errors in judgment. We counter this by sticking to our investment process of properly selecting a diversified group of companies that have attractive risk/return profiles, honest and capable management and, perhaps most importantly, sell at a price that allows for a sufficient margin of safety.

Very sincerely,

The Evans Team