| Index | Q1 2021 |

|---|---|

| S&P/TSX Composite (C$) | 8.05% |

| S&P 500 (US$) | 6.17% |

| S&P 500 (C$) | 4.87% |

| MSCI EAFE (US$) | 3.48% |

| MSCI EAFE (C$) | 2.20% |

| FTSE TMX Universe Bond Index (C$) | ‐5.04% |

| C$ / US$ | 1.2732 to 1.2575 (+1.25%) |

* Index returns are total returns, including dividends.

A STRONG SHIFT

The substantial shift from popular growth stocks to downtrodden value investments that began in November of last year continued in the first quarter of 2021. Encouraged by accelerating vaccine deployments, investors swiftly turned their attention to so‐called recovery plays, eagerly buying up companies that stand to benefit the most from a return to normalcy.

In the first quarter, the Russell 3000 Value Index returned 11.9% compared to 1.2% for the Russell 3000 Growth index. This outperformance has narrowed the one‐, three‐, and five‐year performance gaps of the Growth index over its Value counterpart, but the disparity is still substantial at 6%, 47% and 83% respectively. Some ground has been made up, but the difference in forward price‐to‐earnings multiples of the Value and Growth indices is still comparable to that of the tech bubble of the late‐1990s.

We have also seen a more broad‐based rally in share prices over the last few months, with the S&P 500 equal‐weighted index outperforming its cap‐weighted counterpart by 6% year‐to‐date, and by 16% over the last year. That is to say, the average stock in the S&P 500 performed better than shares in the largest companies – a distinct about‐face after a long period of outperformance by a select few large capitalization technology companies.

Cumulative Returns

S&P 500 Cap‐Weighted S&P 500 Equal‐Weighted

| YTD | 6% | 12% |

| 1‐Year | 56% | 72% |

| 3‐Year | 59% | 52% |

| 5‐Year | 113% | 99% |

| 10‐Year | 268% | 242% |

As a result of this recent outperformance by smaller companies, the 10 largest companies in the S&P 500 now only represent 27% of the total value of the index, down from the historic high of 33% reached at its peak last year. This proportion is still well above historic norms, however.

RISING INFLATION EXPECTATIONS AND RISING YIELDS

The growing expectation that the economic recovery will be faster than previously thought has in turn dramatically increased the outlook for inflation, which has been unusually subdued for much of the last decade. Consumers, having been cooped up in their homes for over a year, unable to spend and supported by unprecedented levels of fiscal stimulus, have amassed a level of personal savings unseen in nearly 50 years. These savings, now sitting in bank deposits, could be rapidly deployed as economies reopen and consumers race back to the stores.

Many expect that the surge in demand caused by reopening will be met with relatively inelastic supply in the short term, leading to increased prices for goods and services. Predictions of a significant jump in inflation have had a notable effect on long‐term bond yields. 30‐year U.S. Treasury yields have risen from 1.3% to 2.4% over the last year while 30‐year Government of Canada yields have risen from 1.2% to 2.0% in just the first three months of 2021. These yield increases have taken place despite both the U.S. Federal Reserve and the Bank of Canada remaining publicly adamant about their commitment to low interest rates and monetary policy easing.

This upward move in yields has led to significant price declines for the government bonds with the longest maturities. For example, the price for the U.S. Treasury bond maturing in February 2051 has fallen by 10% year‐to‐date, while the price for the 30‐year Government of Canada bond issued last December has decreased by 17%. Since our fixed income portfolios are shorter in duration (i.e. maturity) compared to our bond benchmark, the rise in longer‐term rates has significantly contributed to the outperformance of our fixed income portfolio this year.

Rising long‐term yields have had a notable effect on the market’s pricing of equities. Many investors have come to think of some equities as government bond proxies, given their durability and long runways, and as a result ascribe high prices and multiples of earnings to these shares. Higher rates have a more negative impact on the valuations of faster growth companies, which derive most of their value from earnings far into the future: compare this with slower growth companies that derive most of their value from earnings in the near future.

REVISITING A LONG‐TIME HOLDING

A key defense against the prospect of rising interest rates is to insist on an adequate margin of safety for each of our holdings. We always evaluate prospective investments based on the returns that they are likely to deliver, regardless of the interest rate environment. An illustration of this line of thinking is our investment in BMW1, as described below.

Despite the prevailing narrative that BMW is an old economy company soon to be disrupted, BMW has been consistently profitable, even in 2020, investing heavily in new technologies that will position the company well in a future of electric vehicles. BMW spends over €6 billion on research and development every year, with the majority of those funds devoted to new electric propulsion systems. This spending is the highest of any of the automotive original equipment manufacturers (OEMs) as a proportion of their net sales, and even higher than that of Tesla, the current electric vehicle leader.

These huge investment outlays have started to reap benefits: today, BMW is the fourth‐largest seller of electric vehicles globally, and its share of electric vehicle deliveries last year was more than 8%. The company plans to have 25 fully electric models available by 2023, up from just five at the end of 2020.

We believe that BMW can leverage these technological advances, its longstanding positioning as a premium brand, and its strong dealership network to continue to be one of the few prominent OEMs in the new world of transportation. In the meantime, BMW is not resting on its laurels with its traditional business, as it continues to improve the fuel efficiency of its existing internal combustion engine (ICE) fleet.

Currently, BMW has a market capitalization of €57 billion. The company aims for an 8‐10% operating margin and at least a 40% return on capital employed in its Automotive business, and a 14% return on equity in its Financial Services business. This suggests that the company should earn at least €7 billion and €2 billion before tax from the two businesses, respectively. Moreover, the company is also well capitalized, with net cash in its Automotive segment of more than €9 billion.

At its current price, BMW is trading at just six times normalized pre‐tax earnings, a multiple well below that of its OEM peers and one that we believe strongly undervalues the company. An additional benefit to our investment is that we own BMW’s preference shares. These preference shares are less liquid than the common shares and have fewer voting rights, but have identical economic interests. Today, these preference shares trade at a near 25% discount to the main common shares, providing us with an even lower price for purchase and an additional layer of safety.

POSITIONING FOR THE FUTURE

While security market prices have rallied significantly over the past year, we continue to believe that our portfolios remain relatively well positioned for the future. By design, our bond portfolios have typically been short in duration since we have been unwilling to lock in low returns for long periods. This has negatively impacted our performance over the past few years, but gives us the option to reinvest at higher yields and longer maturities as rates rise.

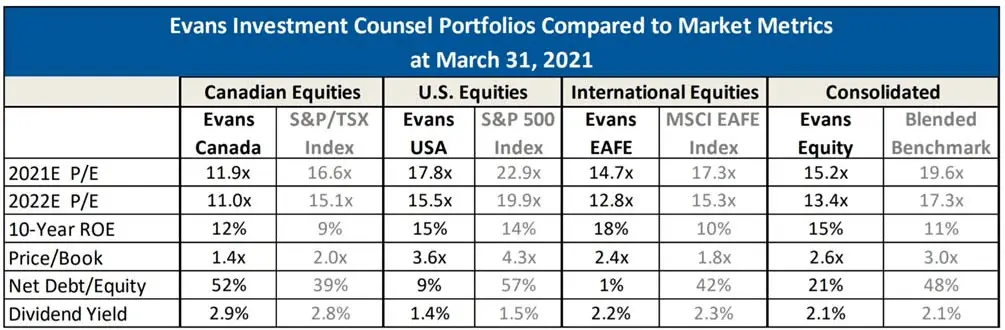

We continue to be very cognizant of the prices that we pay for stocks. Despite the strong run‐up in prices, our equity portfolios remain modestly priced compared to the broader indices, while at the same time consistently generating higher returns on equity and carrying lower levels of debt, as shown below.

Unpopular as it may sometimes be in the short run, we believe that this disciplined approach to selecting investments and being highly mindful about the prices we pay will lead to satisfactory returns while assuming substantially lower risk over the long run.

Thank you for your continued confidence and support,

The Evans Team