| Index | Q1 2022 |

|---|---|

| S&P/TSX Composite (C$) | 3.8% |

| S&P 500 (US$) | ‐4.6% |

| S&P 500 (C$) | ‐6.0% |

| MSCI EAFE (US$) | ‐5.9% |

| MSCI EAFE (C$) | ‐7.3% |

| FTSE TMX Universe Bond Index (C$) | ‐7.0% |

| C$ / US$ | 1.2678 to 1.2496 (1.5%) |

* Index returns are total returns, including dividends.

ONE CRISIS FOLLOWING ANOTHER

Just as the world was finally beginning to move on from the COVID‐19 pandemic, it was hit by the shock of Russia’s invasion of Ukraine in late February. The ensuing violence and tragic humanitarian crisis quickly spurred many of the world’s nations to impose severe sanctions on Russia and its economy. These measures, along with the chaos of war, threw global markets into turmoil once again and exacerbated many of the challenges already facing a global economy still reeling from the fallout of the pandemic.

War and sanctions propelled inflation to even higher levels nearly everywhere in the world. The speed at which the cost of basic necessities such as gasoline and food rose caught the world’s central banks off guard, and led to a renewed sense of urgency to speed up rate increases and the unwinding of the massive amount of monetary stimulus undertaken during the pandemic. All this had an immediate effect on resetting investor expectations, which in turn led to a significant shift in asset prices.

In equities, the S&P 500 has returned ‐4.6% year to date. The decline itself has been only moderate: the really substantial change has been what investors favour and disfavour within the index. Energy, the most underachieving sector of the last decade, delivered a whopping +39% return in the quarter; meanwhile, the two best performers of the last ten years, technology and communication services, did the most poorly, returning ‐8.4% and ‐11.9% respectively. This sudden reversal of what had been the norm for over a decade serves as a stark reminder of just how fast market sentiment can shift.

There has been a similar turnaround of decades‐long trends in fixed income markets, where the risks associated with long duration bonds with rock‐bottom yields have suddenly become far more apparent. Government bonds, for years among the most favoured of fixed income asset classes, have been hit the hardest. Just a 0.5% increase in yields over the last three months has been enough to drive year‐to‐date returns for 30‐year U.S. Treasury bonds to ‐11.4%. Similarly, investment‐grade bonds, those issued by companies perceived to have the least credit risk, were the worst‐performing of all corporate bonds. In both government and investment‐grade bonds, yields were so low at the beginning of the year that even a modest shift in rates was enough to lead to significant price declines.

THE GRAVITATIONAL PULL OF RISING INTEREST RATES ON ASSET PRICES

Over much of the past decade, many investors valued assets assuming interest rates would remain low forever. Indeed, with interest rates effectively at zero, a near infinite value could be theoretically ascribed to assets that earned virtually nothing but promised large windfalls at some point in a fanciful future. These assumptions were compounded by the massive amount of liquidity injected into markets by central banks, leading to immense amounts of cash chasing a finite number of favoured assets, helping push speculation and prices to absurd levels.

In just a few short months, the widespread belief that inflation and interest rates would remain low forever has been shattered. Investors are now suffering a rude awakening and beginning to feel the downward pull of higher rates on asset prices for the first time in well over ten years. The S&P 500’s forward price‐to‐earnings ratio has fallen from 22 times to 20 times over the last year, and valuations for the priciest sectors have fallen even more: forward price‐to‐earnings ratios for the consumer discretionary, technology and communication services sectors have contracted by as many as eight multiple points.

The loudest wakeup call has been reserved for assets whose prices rose the fastest amid the euphoria. Small‐capitalization growth stocks, the most speculative group of companies, have seen their price‐to‐earnings multiples more than halve in just a year – from 86 times to 40 times. With investors now realizing that faraway profits may be just a pie in the sky fantasy, they have increasingly spurned many of the money‐losing, pre‐revenue companies that popped up by the dozen over the last few years.

WHEN THE PUNCHBOWL IS TAKEN AWAY

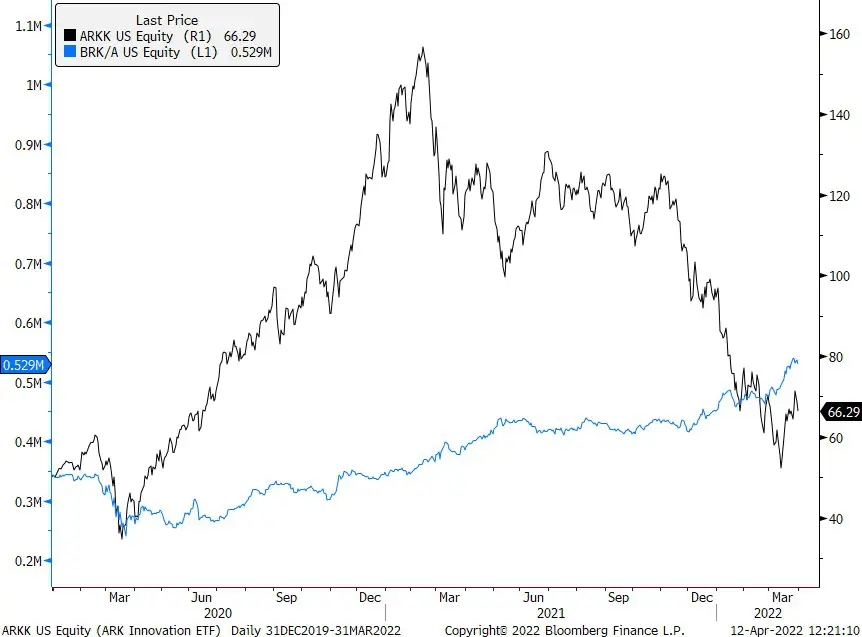

Perhaps nothing captures the current state of affairs better than the juxtaposition of the recent performance of the ARK Innovation ETF against that of Berkshire Hathaway. Composed of marginally profitable, money‐losing, high revenue‐growth companies, ARK rose to immense popularity amid the momentum boom over the last two years. From the beginning of 2020 to its peak in February 2021, ARK’s share price more than tripled. Meanwhile, Berkshire Hathaway, the large conglomerate founded by Warren Buffett and a position we have held for a long time, saw its stock price meander, rising just 5% over the same time frame.

As ARK rose higher and higher amid the speculative fervour and Berkshire, a paragon of value investing, seemed frozen in stasis, commentators in increasing numbers began to assert that a new method of investing had arrived and that the “old way” of investing, that is to say appraising businesses on their earning potential and paying sensible prices, was now outmoded and passé. Such arguments were strongly reminiscent of the tech bubble of the late‐1990s, when the prevailing wisdom at the time paid little to no heed to business fundamentals.

Under the guise of these “new world” pronouncements, many market participants were finding ways to rationalize the extreme price momentum driving many of these stocks ever higher. So long as the party continued, it seemed nearly irresistible for many to join. The quandary, of course, is knowing exactly when the party will stop, and the punchbowl will be taken away.

Since that high‐water mark, reached in February 2021, the party has stopped and ARK has fallen 58%. Meanwhile, ho‐hum, slow and steady, unglamorous Berkshire has risen by 45%. The reversal has been so stark that Berkshire has now transformed an underperformance compared to ARK of 211% to an outperformance of 22% since the beginning of 2020.

REMAINING FOCUSED ON OUR PHILOSOPHY AND PROCESS

The relatively dramatic price movements mentioned above reveal the peril of paying absurd prices for stocks and accepting low yields on bonds. For us, we have long been agnostic about macroeconomics but remained vigilant about the prices we pay for assets, regardless of the interest rate environment. In our view, the best way to guard against changing winds is not to try to predict which direction the winds are shifting but to remain disciplined, insist on a substantial margin of safety, and neither overpay for nor accept low returns on investments.

Our equity holdings currently trade at 13 times their current year’s expected earnings, which is in line with where our equity portfolios have historically traded. This translates to an earnings yield of nearly 8%, higher than prevailing inflation rates and well above long‐term government bond yields. In addition, unlike bonds, our equity holdings are likely to grow their earnings over time (especially if inflation persists) which means that our companies will see their earnings yields expand on current market prices.

In fixed income markets, we have long maintained a desire to keep duration low and have refused to lock in low yields over the long run. We believe that there are now considerably more opportunities to deploy capital in bonds at acceptable returns than there were at this time last year. It has been years since we have seen yields higher than 4% for even non‐investment‐grade bonds. Today, we are finding investment‐grade issues of short duration that approach that level.

While security markets have been volatile lately, we feel comparatively better about the future return profile for both our equity and fixed income holdings than we did during the tranquil and pricey markets of last year. Stock valuations have moderated closer to their historical range and bond yields have improved substantially, setting up conditions for better long‐term return prospects.

Thank you for your continued confidence and support.

The Evans Team