| Index | Q1 2023 |

|---|---|

| S&P/TSX Composite (C$) | 4.6% |

| S&P 500 (US$) | 7.5% |

| S&P 500 (C$) | 7.4% |

| MSCI EAFE (US$) | 8.5% |

| MSCI EAFE (C$) | 8.4% |

| FTSE TMX Universe Bond Index (C$) | 3.2% |

| C$ / US$ | 1.3544 to 1.3533 (0.1%) |

* Index returns are total returns, including dividends.

NOT BANKING ON ANOTHER 2008

Interest rates continued to rise higher this quarter. This brought fresh concerns for the economy as a whole and, in particular, liquidity in the banking sector. Not surprisingly, taking rates from 0.25% to 4.75% in the past year removed a lot of liquidity from the system, and we are now beginning to see the consequences.

As Warren Buffet once famously said, “Only when the tide goes out do you learn who has been swimming naked.” This quarter we saw who had forgotten their swimsuits at home when Silicon Valley Bank, Signature Bank, and Credit Suisse all became insolvent, representing the largest bank failures since Washington Mutual in 2008. Their collapse was partially due to the higher interest rate environment but also to poor risk management, as these banks were mismatching short‐term deposits (liabilities) with long‐term Treasury bonds (assets). The long‐term assets were recorded as Held‐to‐Maturity – that is, carried on the books at cost – but were trading in the market at lower prices. When the banks were forced to liquidate significant amounts of these assets, they took heavy losses.

In the case of Silicon Valley Bank, unbeknownst to the general public, a handful of venture capital funds controlled a great many of the bank’s 35,000 customers. The venture capital funds instructed their portfolio companies to move all deposits from Silicon Valley Bank, triggering a forced selling of their Held‐to‐Maturity assets at a loss to meet the withdrawal requests. Thus began a run on the bank. Many small bank customers followed suit, and similarly moved their deposits from regional banks to larger ones.

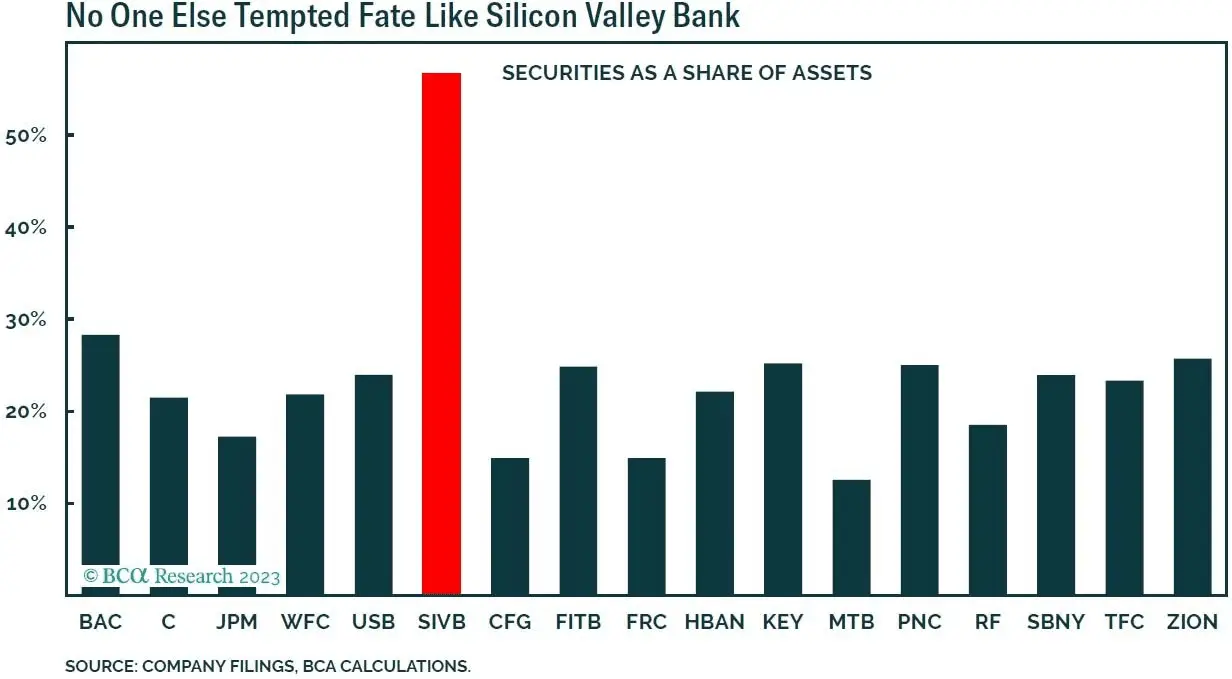

The collapse of Silicon Valley Bank shed a light on the risk of having uninsured deposits at smaller banks (in Canada, deposits are insured up to C$100,000 and in the U.S. up to US$250,000). A few factors have since contributed to the stabilization of customer deposits. In an effort to help stem the panicked outflow of deposits from the regional banks, larger banks like JPMorgan, Bank of America, and Wells Fargo reduced the interest rate on their deposits to 0.01% to dissuade customers from moving more funds to them. Meanwhile, the U.S. government promised that all deposits at Silicon Valley Bank beyond those insured by the Federal Deposit Insurance Corporation (“FDIC”) would be reimbursed. Additionally, it is now more widely understood that Silicon Valley Bank, with its disproportionate exposure to Held‐to‐Maturity securities and more narrow deposit base, was in a significantly riskier position than other banks. The chart below shows that Silicon Valley Bank held 57% of its assets in securities, more than double any other bank despite a less stable sticky and narrower deposit base.

While we are still not out of the woods, we do not believe that the banking sector as a whole will be as severely impacted as it was fifteen years ago. These events were confined to a few specific banks, and not sparked by a system‐wide issue like in 2008.

FINDING STRENGTH IN SIZE

At Evans, our goal is and always has been to own resilient companies with strong business models and mitigated downside risk. As such, we favour larger, more diversified banks integral to their country’s economy. It doesn’t mean they aren’t too big to fail, as we saw in 2008, but it is much less likely. This makes the risk/return profile much more enticing.

Compared to Silicon Valley Bank, the U.S. banks we hold have more diverse deposit bases, lower percentages of assets in securities, and have better matched the durations of their assets and liabilities. We also hold Canadian banks, which are more regulated than U.S. banks to mitigate the possibility of bank failure. Moreover, Canadian banks are more oligopolistic, resulting in better pricing power and less hyper‐competitive behaviour which can increase risk‐taking.

Although our companies are well positioned to recover from this headwind, this event does put some strain on the entire global economy, and there is continuing debate whether interest rates will continue to increase to battle inflation, or whether governments will wait to see if the waters calm on their own.

NAVIGATING A MACRO‐FOCUSED MARKET

Much of the recent market volatility continues to be influenced by macro news. In Q1 alone, the S&P 500 index rose 9.3% from 3,824 to 4,179, tumbled back down 7.8% to 3,855, and then bounced back up 6.0% to finish at 4,085. It is unlikely the collective true fundamental value of the top 500 U.S. companies fluctuated that drastically in only three months: these swings in the market seem to be driven by sentiment. For example, the final 6% rise was immediately following the failure of Silicon Valley Bank. The newspapers were full of headlines in the wake of the bank failure saying that the Fed might be hesitant to raise interest rates further, implying asset prices would go up.

Only very seldom do market participants accurately predict market movement. We prefer to remain steadfast in our strategy that has performed well over decades of different market cycles and event‐driven market swings: we continue to hold companies with better operating metrics, less leverage, and that are trading at cheaper prices than the average market company.

WHERE WE CONTINUE TO FIND VALUE1

Air Canada Bonds

Following the drop in fixed income prices last year, we have been able to uncover more opportunities to capture good yields on fixed income. For example, the 4.62% Air Canada 08/15/2029 bonds provide a yield‐to‐maturity of 6.5%. These bonds are not purchased by many institutional investors because their investment mandates preclude them from buying them, due to their non‐investment grade BB‐ rating. However, these are senior secured bonds backed by strong collateral – namely, substantially all the company’s international routes, airport slots, and gate leaseholds. Our belief is that Air Canada as an entity is very unlikely to fail, given that it is a vital component of Canada’s transportation infrastructure. Even in the unlikely event that it did fail, our bonds are protected by their collateral. In our opinion, these bonds offer an attractive yield with minimal risk.

Berry Global Stock

One example of where we continue to find value in equities is Berry Global. Founded in 1967, Berry Global is a worldwide manufacturer of plastic packaging products with more than 70% of its sales coming from stable end‐markets such as food, beverage, home, and personal care. Berry serves a broad base of 20,000 customers from 300 plants in 50 countries. Berry’s significant size and scale give it a distinct advantage when it comes to purchasing resin, which accounts for 50% of its costs of goods sold.

While plastic packaging is somewhat out of favour today for environmental reasons, it does serve a vital function in society. Plastics compared to alternative packaging products take significantly less energy to make, and for perishable food items delay spoilage by 4‐5 days. The company has also set a goal to achieve 100% recyclable, compostable, or reusable packaging by 2025.

Berry has an established track record of revenue and earnings per share (EPS) growth, and trades at a significant discount to its peers. The stock price has tripled in the past decade, but its EPS has increased six‐fold. It continues to operate in a fragmented industry and is a disciplined acquirer, so we believe there is plenty of growth ahead with decades of consolidation yet to come.

We see multiple additional opportunities for Berry to unlock shareholder value, including increasing its share repurchases now that its debt is within its target range. The company is considering sale/leaseback transactions to monetize their roughly $2 billion in real estate assets (which represent roughly 30% of Berry’s market value). Our belief is that the company is inexpensive at 7x earnings, can continue to compound earnings at a reasonable rate, and has many as yet unexplored ways to create further benefits for its investors.

As we’ve done for the past 35 years, we focus on understanding the fundamentals of businesses as opposed to bending and swaying in the macro news winds. Our portfolios today hold companies that are much cheaper, more profitable, faster growing, and use significantly less financial leverage than the market average, as shown below. We will continue to use our resources to uncover great investment opportunities for our clients, and expect that will benefit them over the long term.

Thank you for your continued confidence and support.

The Evans Team