Index |

Q1 2026 |

|---|---|

S&P/TSX Composite (C$) |

3.9% |

S&P 500 (US$) |

-4.3% |

S&P 500 (C$) |

-2.7% |

MSCI EAFE (US$) |

-1.2% |

MSCI EAFE (C$) |

0.4% |

FTSE TMX Universe Bond Index (C$) |

0.2% |

C$ / US$ |

1.3706 to 1.3939 (-1.7%) |

* Index returns are total returns, including dividends.

WEATHER PATTERNS

“Climate is what you expect. Weather is what you get.”

– Edward Lorenz

There is a well-known distinction in science: weather is what we experience day-to-day, while climate affects the environment over time. A sudden storm can dominate the day’s forecast, but does little to change the prevailing climate. Markets often behave the same way, pulled between short-term events that demand our immediate attention and longer-term forces that shape the future.

The “Weather”: The Geopolitical Storm

The most visible pressure this quarter came from the escalating conflict in the Middle East. As tensions rose, so did oil prices, driven by concerns surrounding potential supply disruptions through the Strait of Hormuz, a critical artery for global energy. While no prolonged disruption has yet materialized, markets have been quick to price in the risk. The result was a sharp move higher in energy prices, which acted as both a tailwind and a headwind depending on where you looked.

Energy producers like Shell plc benefited from stronger pricing, while sectors more sensitive to costs, such as transportation, industrials, and certain consumer businesses, faced immediate pressure. This is typical of commodity-driven shocks. Higher oil prices generally redistribute earnings across the market rather than destroying them altogether, creating short-term winners and losers.

The “Climate”: The AI Transition

Meanwhile, a subtler but arguably more important shift has been unfolding. The continued rise of artificial intelligence (“AI”) has begun to reshape expectations across the software landscape.

Many software companies, particularly those with high valuations built on long-duration growth assumptions, have seen significant declines as investors reassess their positioning in an AI-driven world. Former market darlings including Salesforce, FactSet, Adobe, and Thompson Reuters have seen their stock prices plummet 30% or more over the past twelve months.

This repricing reflects uncertainty rather than fundamental business failure. How durable are existing software models? Will AI compress margins, or expand them? Which companies will adapt? Which will fall behind? When the answers are unclear, markets tend to err on the side of caution, reminding us how drastic the decline can be when expectations are high.

Opportunity in the “Magnificent Seven”

This uncertainty has affected even the seemingly indestructible “Magnificent Seven”. The valuations of companies including Microsoft, Amazon, and Meta have all dropped to levels rarely seen in their recent history, trading at 20x price-to-earnings ratio (P/E), 24x P/E, and 18x P/E respectively. Within the broader context of the S&P 500, which is currently trading at 19x P/E, the implication is that these dominant, fast-growing companies are roughly worth only the price of the market-average company today. For long-term investors, however, these declines are often where opportunity begins: not when uncertainty is resolved, but when it is being factored in.

Taken together, geopolitical disruption and technological transition highlight an important reality: markets are constantly adjusting to both the present and the future. One is immediate and reactive; the other gradual and forward-looking. But both create the same outcome of dispersion.

If, today, geopolitics represents the “weather” of markets – sudden, visible, and often unpredictable – then technological change is the “climate,” shaping the environment in which businesses operate. While storms may pass, climate endures. As investors, our focus remains on positioning portfolios for that longer-term climate, while maintaining the discipline to look beyond the noise of the weather.

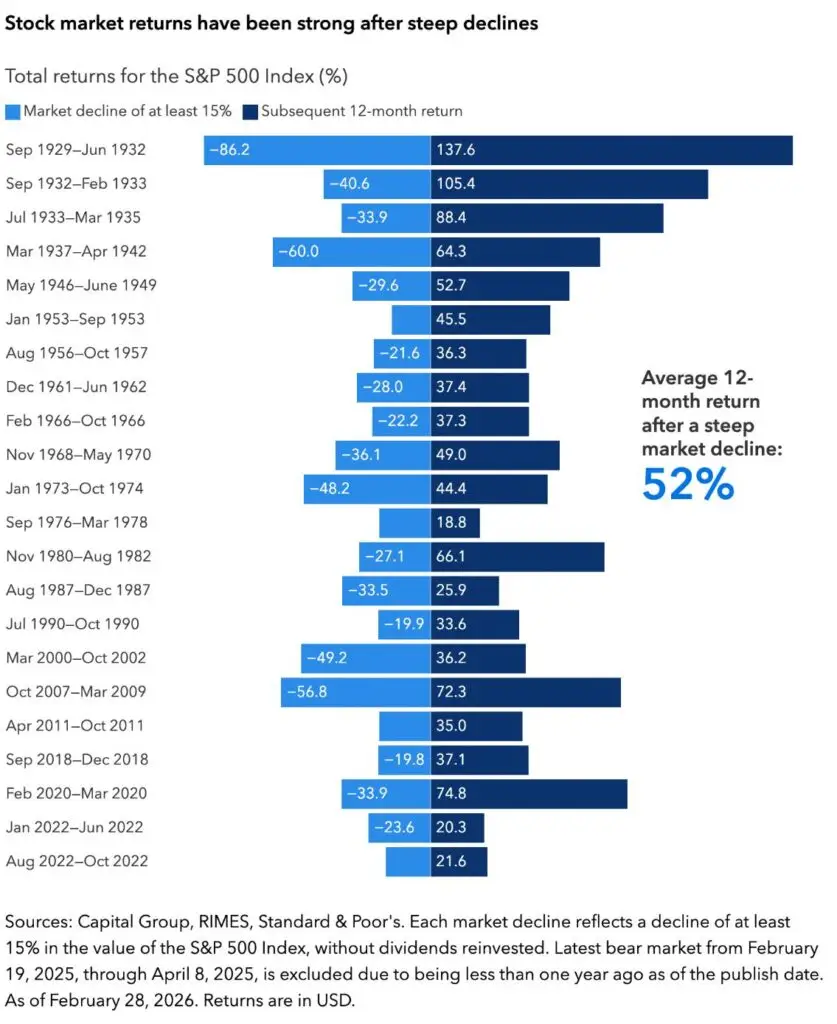

Periods of stormy weather test investors. When headlines dominate and markets move unevenly, the instinct is often to adjust, to respond, to “do something.” Yet, history consistently shows that the greatest risk to long-term returns is not volatility itself, but the decisions investors make in response to it. Missing even a small number of the market’s strongest days, often clustered around periods of heightened uncertainty, can have a significant negative impact on long-term outcomes.

While it can feel counterintuitive, the most rational course of action is often inaction: to remain disciplined, avoid listening to short-term noise, and allow the underlying strength of well-chosen businesses to compound over time.

FINDING OPPORTUNITY IN A CHANGING ENVIRONMENT

Amazon¹ is one of the most recognizable businesses in the world, but its current form is the result of nearly three decades of continual reinvention. Founded by Jeff Bezos in 1994 as an online bookstore, the company has since evolved into a global platform spanning e-commerce, cloud computing, digital advertising, and logistics infrastructure.

Today, Amazon’s business can be broadly understood as three primary engines:

- E-commerce — North America & International: The company’s largest segment by revenue, which includes first-party retail and third-party marketplace sales. Over time, profitability has improved with greater scale and growing third-party marketplace services while continuing to invest in faster delivery and international growth.

- Amazon Web Services — AWS: This is the company’s cloud computing division and its most profitable segment. AWS is the market leader in the sector, with revenue roughly 70% greater than its next largest competitor. AWS provides IT infrastructure – compute, storage, and software tools – more quickly and efficiently than building in-house, making it a key enabler of digital innovation, including AI.

- Advertising & Other Services: A rapidly growing segment, Amazon’s advertising business leverages its vast consumer data and marketplace traffic to deliver extremely high-margin revenue.

What makes Amazon particularly compelling as an investment is the interplay between these segments. Its logistics scale supports e-commerce efficiency, which in turn drives marketplace traffic, reinforcing its advertising business, while AWS benefits from the massive shift towards AI infrastructure, offering diversification within a single company.

From a valuation perspective, Amazon has become significantly more attractive in recent years, dropping from a median 10-year P/E of 44x to 24x. At the same time, AWS’ growth, while slightly dipping from peak levels, remains robust and continues to benefit from long-term trends such as online shopping, cloud adoption and artificial intelligence infrastructure.

In our view, Amazon represents a high-quality business with improving profitability, multiple long-term growth drivers, and a valuation that has, for perhaps the first time in its history, reached a level we believe is a strong risk/return relative to the broader market.

¹ Some clients may not hold Amazon due to asset mix or timing.

RECOGNIZING ALTERNATIVES

A critical aspect of disciplined investing is not only knowing what to buy, but also when to sell. Our approach is grounded in two primary principles governing when to exit a position: (1) if the market price meets or exceeds our estimate of intrinsic value, or (2) if our underlying investment thesis changes. In the case of ATCO², our decision was driven by the former.

ATCO is a Canadian-based infrastructure and utilities company with an operating history dating back to 1947. Through its subsidiaries, the company operates in electricity and natural gas transmission and distribution, energy infrastructure, and modular structures. Its utility operations, particularly through Canadian Utilities, have historically provided investors with stable, regulated earnings and predictable cash flows.

This stability has made ATCO an attractive holding to us at various points, particularly when purchased at a discount to its intrinsic value. The business benefits from essential service characteristics, long-lived assets, and regulatory frameworks that support reasonable returns on capital. However, these same characteristics also tend to weigh down long-term growth. Utilities, by nature, are not high-growth businesses. Their value is derived from steady cash flows, not rapid expansion. Thus, valuation discipline becomes especially important.

Since 2023, ATCO’s share price appreciated from a price-to-book valuation of under 1.0x to over 1.4x. In our assessment, while the business itself remains sound, the margin of safety that initially attracted us to the investment had diminished, and there were other opportunities that we felt offered more attractive risk/reward characteristics.

Selling in these situations can be challenging. It can involve parting with a stable, well-run company. However, capital allocation is about opportunity cost. By exiting positions where the upside is limited, we create room to redeploy capital into investments with more favourable risk/reward profiles, such as our recent investment in Amazon.

In this case, the decision was not a reflection of deteriorating business quality, but rather an acknowledgement that ultimately investing is about recognizing the opportunity cost of capital.

“All intelligent people should think primarily in terms of opportunity cost. When deciding whether to do something compare it with the best opportunity you have.”

— Charlie Munger

Thank you for your continued confidence and support.

The Evans Team

² Some clients may not have held ATCO due to asset mix or timing.