| Index | Q3 2020 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 4.7% | ‐3.1% |

| S&P 500 (US$) | 8.9% | 5.6% |

| S&P 500 (C$) | 6.6% | 8.4% |

| MSCI EAFE (US$) | 4.8% | ‐7.1% |

| MSCI EAFE (C$) | 2.6% | ‐4.6% |

| FTSE TMX Universe Bond Index (C$) | 0.4% | 8.0% |

| C$ / US$ | 1.3628 to 1.3339 (2.2%) | 1.2988 to 1.3339 (‐2.6%) |

* Index returns are total returns, including dividends.

A HIGHLY UNEVEN RECOVERY

The world’s economies continue to recover following the unprecedented lockdown orders in the spring, and equity markets have broadly regained the losses sustained during the nadir in March. While the stock indices themselves have largely recovered, the gains have not been evenly distributed. Stock prices of companies relatively unaffected by the lockdown have since soared past their pre‐pandemic levels, while those of other sectors have remained depressed.

The disparity between the best and worst performing sectors has been significant. Year to date, returns in growth sectors such as e‐commerce have been 60%, whereas returns in heavily out‐of‐ favour sectors such as energy or retail have been ‐40% or even lower. Technology has no doubt been the outlier this year and its weighting in market indices has risen to nearly the record levels seen during the heady days of the 1990s tech bubble. Today, the Technology sector’s weight in the S&P 500 stands at 39%, even while the sector itself generates economic production amounting to only 6% of U.S. GDP.

Within the Technology sector, three quarters (and 29% of the S&P 500) is comprised of just 10 companies that are collectively valued at 35x forward earnings. This disproportionately high weight of a select few large capitalization technology companies that are currently in vogue has pushed the S&P 500’s price‐to‐forward‐earnings multiple to 22x, well above that of its 25‐year average and that of stock market indices everywhere else in the world.

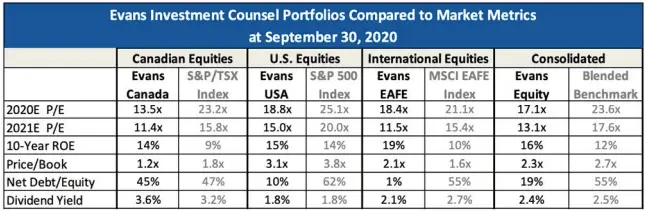

The strong divergence in market performance this year has pushed our equity holdings to their cheapest levels relative to that of benchmark indices in years. On a price‐to‐forward‐earnings basis, our consolidated equity holdings currently trade at 13x, compared to 18x for the blended benchmark. While some people equate cheapness with lower quality or higher risk, we believe that this is not the case when evaluating our holdings. In aggregate, our holdings are, and have continued to be, more profitable overall (as measured by higher returns on equity), while employing substantially less leverage.

OUT OF FAVOUR SECTORS: AUTOS AND FINANCIALS

While the prices of many of the high‐flying “new economy” stocks reflect assumptions of an increasingly pie‐in‐the‐sky nature about their future prospects, the prices of stocks in other sectors suggest reticent views about their future ability even to tread water. Two examples of the latter are auto‐related companies and banks, both of which are sectors that have dramatically underperformed broader market indices this year and have relatively sizable weights in our portfolios.

Some of the auto and auto supplier companies that we own currently trade at single‐digit multiples of normalized earnings. Such a trading multiple seems to suggest perpetual decline in earnings power in the future, even though many of these companies have maintained leadership in their fields for decades. Disruption in the auto business has featured strongly in the recent public narrative, chiefly manifesting itself in the form of one company (Tesla), whose market capitalization has vaulted past that of the top two auto manufacturers combined, even as it makes less than 5% of either’s production in any given year.

Nonetheless, disruption has been the lone constant throughout the history of the auto industry. Change and innovation are inevitable and the auto companies that we own are highly cognizant of the fact. They are hardly waiting around; rather, in response, they have invested considerable capital, both human and financial, in future methods of propulsion, particularly electric. We believe that the advantages that these companies have accrued over the years as leaders in their industries will likely make them highly competitive players in the decades to come, even as their stock prices would suggest all but certain impending doom.

We also maintain a high weighting in banks, some of which trade at low double‐digit multiples of current recession‐level earnings. Broadly speaking, the banks that we own have weathered the current downturn remarkably well, and despite setting aside record reserves for credit losses over the last two quarters, have even increased their capital levels during the pandemic. In Canada, banks have been remarkably resilient, helped by an oligopolistic industry structure that has yielded consistently conservative behaviour among the incumbents. In the U.S., the banking industry is transforming to resemble something more like Canada’s: the largest banks have advantages in scale and resources that smaller banks cannot match, catalyzing a long runway for consolidation.

Currently, many market participants have been apprehensive about investing in banks due to near‐term concerns about credit losses and ultra‐low interest rates, leading to low prices for their stocks. We take comfort in the exceptionally strong capital positions of the banks that we own, their conservative underwriting, and their growing economic moats. Over the long term, we believe that the economy will recover and normalize, yielding a more constructive interest rate environment than currently exists. In the meantime, we believe that our ownership in banks is an attractive investment, even assuming below‐average earnings power in the short to mid term.

AND A NEW BUY

Another example of a sector in which recent macro uncertainty has had an enormous effect on stock prices has been health care. COVID‐19 and the upcoming battle in U.S. politics have brought renewed attention to the issues of health care in the country. In recent years, drug pricing has been a particular focal point in the contentious debate, and now it has been further magnified by the current pandemic. Fears about wholesale changes to drug approval, pricing and administration negatively affecting the industry have been overblown – in our view – and have allowed us an attractive entry‐point to add a pharmaceutical company, Bristol‐Myers Squibb, to client portfolios.1

Bristol‐Myers Squibb is a global pharmaceutical company, primarily known for drugs that treat strokes, cancer, and rheumatoid arthritis. The company primarily manufactures branded drugs, that is, drugs that have exclusivity for approved indications. Companies that sell branded drugs have a limited period of exclusivity in which they can charge monopolistic prices to recoup the investment required for research and development and for the company to earn a sufficient return. We believe that the bulk of Bristol‐Myers’s branded drugs have a fairly long runway of exclusivity and that the company has an attractive pipeline of drugs and biologics in various stages of clinical trials.

Despite the relatively high visibility of earnings for at least the next four years, Bristol‐Myers currently trades at just 8.5x its next year’s forecasted earnings, notably below its peers. With its current line of drugs, Bristol‐Myers can grow EPS by nearly 10% through 2024, after which it will start to lose exclusivity for a few of its branded drugs. This, combined with fears about drug pricing and political uncertainty, has led to a depressed share price, which now tacitly assumes perpetual decline of the company’s earnings stream over time.

In our view, such an outcome is unlikely considering the strength and longevity of the company’s current roster of branded drugs, their existing pipeline, and their history of developing and acquiring new drugs. We believe that the strength of its existing product line provides an attractive and growing earnings stream to sufficiently bridge the gap until existing drugs in the pipeline ultimately come to market.

NO ONE CAN KNOW WHAT HAPPENS IN THE SHORT TERM

We have often stressed that we do not know, nor do we believe that anyone else can know, what stock prices will do in the short term. In the short term, stock prices are dictated far more by emotion and sentiment than by the underlying business’ fundamentals. It is only over the long term that a stock’s price and its underlying fundamental value begin to converge. As Benjamin Graham famously said long ago, “In the short term, markets are voting machines but in the long term, they are weighing machines.”

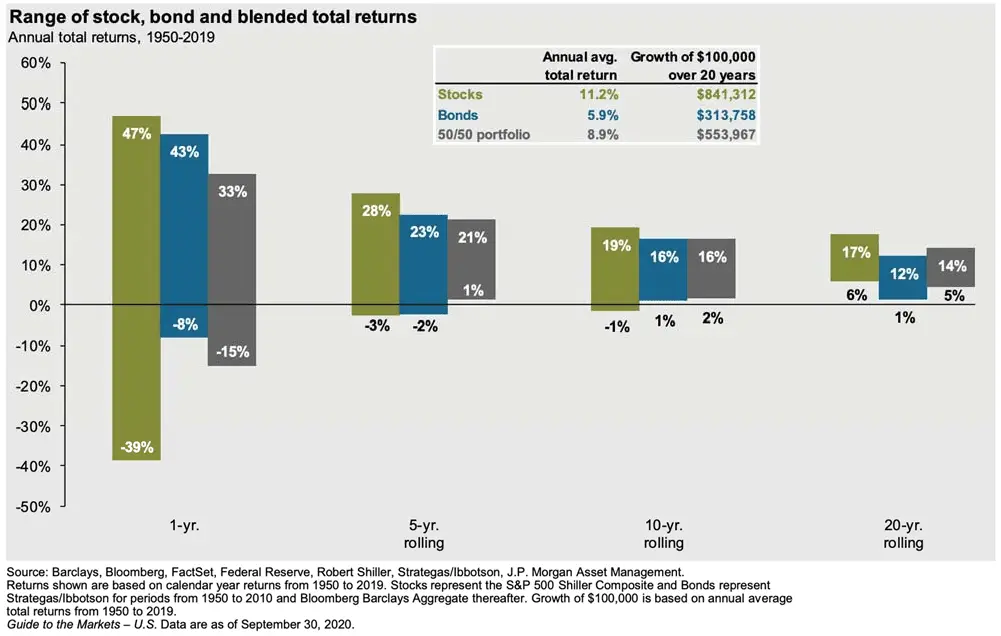

To illustrate this point, consider the following chart that shows the range of annual returns that stocks (as represented by the S&P 500), bonds and a 50/50 portfolio of each produced over 1‐ year, 5‐year, 10‐year and 20‐year rolling time periods over the last 70 years ending in 2019.

Over 1‐year time horizons, the range of annual returns has been extraordinarily wide with equities returning anywhere between ‐39% to +47%, bonds ‐8% to +43%, and a 50/50 portfolio ‐15% to +33% over the past 70 years. With such a wide range of different outcomes, it is understandable why many think of securities markets as casinos, where fortunes can twist and turn inexplicably, without reason, and on very short notice.

However, over longer periods, the range of values shrinks considerably. Over 5‐year, 10‐year and 20‐year time periods, annualized equity return ranges tighten from ‐3% to +28% to ‐1% to +19% and to +6% to +17% respectively. Moreover, note that the mid‐point in the 20‐year range is +11%, exactly equal to the average annual return that equities have generated over the last 70 years. Note that this +11% is only slightly above the sum of the index’s long‐term earnings per share growth of +6% and average dividend yield of +4%. Indeed, over long enough time horizons, it is chiefly the business itself that determines the return the investor will receive.

IMPORTANCE OF STAYING INVESTED

The incredibly high variance of short‐term results shows that viewing performance through narrow time windows can be highly misleading. Our own results over time have been no different: we similarly see tremendous variance in our returns over short time periods that contracts over longer and longer periods. The following shows the range of our annualized returns across our Equity, Balanced Growth and Conservative Balanced composites since inception (Q1 1993).

Range Of Annual Returns From Q1 1993 To Q3 2020 Over Rolling Periods

| 1‐Year | 5‐Year | 10‐Year | 20‐Year | |

|---|---|---|---|---|

| Evans Equity Composite | ‐31% to 56% | ‐2% to 28% | 5% to 18% | 7% to 12% |

| Evans Balanced Growth Composite | ‐24% to 48% | 0% to 27% | 5% to 16% | 8% to 12% |

| Evans Conservative Balanced Composite | ‐13% to 45% | 1% to 22% | 6% to 15% | 7% to 11% |

In addition, when examining the range of returns produced, we found that some of our best results were achieved in the periods that followed cycles of our worst performance. In the years following the first quarter of 2009, which marked the end of our worst 1‐year, 3‐year and 5‐year rolling returns, our equity composite generated annualized returns of 45%, 18% and 19% over the following one year, three years and five years, respectively.

These statistics highlight the imperative of staying invested, particularly during times when it feels most difficult to do so. We believe that we encountered just such a test this past March when stock prices were seemingly falling by 10% a day during one particularly spell‐binding week. During such times, it is useful to remind ourselves that in the short‐term anything can happen, but if you can keep a long‐term perspective, the best returns usually follow periods of the worst.

Thank you for your continued confidence and support,

The Evans Team