| Index | Q3 2023 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | -2.2% | 3.4% |

| S&P 500 (US$) | -3.3% | 13.1% |

| S&P 500 (C$) | -1.2% | 12.9% |

| MSCI EAFE (US$) | -4.1% | 7.1% |

| MSCI EAFE (C$) | -2.1% | 6.9% |

| FTSE TMX Universe Bond Index (C$) | -3.9% | -1.5% |

| C$ / US$ | 1.324 to 1.352 | 1.354 to 1.352 |

* Index returns are total returns, including dividends.

SEWARD’S FOLLY

During the 18th century, the North American fur trade was booming. To capitalize on a profitable trade route into North America, Russia had prudently established a settlement in Alaska. However, as the fur trade dwindled, Russia’s interest in the expensive endeavour of maintaining their Alaskan presence was waning. By the mid 19th century, Russia had decided the land was not worth the cost to occupy it, and they sold it to the United States for $7.2 million in gold through a deal negotiated by William H. Seward. At the time, the Alaskan territory was perceived by the American public as an icy wasteland and the deal was heavily criticized, being dubbed “Seward’s Folly.” As it turned out, Russia had sold too early. Over time, Alaska would prove to be abundant with natural resources including fish, minerals, and timber, all of which realized massive value for the United States over the following 150 years.

The story of mistimed sales has been told over and over throughout history. Selling technology stocks in 2002. Selling homes in 2009. Instagram selling itself to Facebook in 2012. Time and again, assets in all manner of sectors have been sold in the middle of crashes – before recoveries, and before adequate time has been allowed to realize their full value. However, so long as the fundamental long-term outlook remains favourable, maintaining a long-term mindset through short-term troughs will most often prove beneficial over time.

Emotions complicate the selling decision, though. It’s human nature to be excited when things are going well and fearful when things are going poorly. Those who win the lottery jump for joy dreaming of their new life, while those who lose their job are nervous about how they will support their family. The same mindset applies to equity markets. Those who see stock prices rise quickly get excited and pile on, while those who see them fall become fearful and sell out. That very behaviour is what creates booms and busts. In addition, news stories can exacerbate fear and panic and cause people to take a shorter-term outlook.

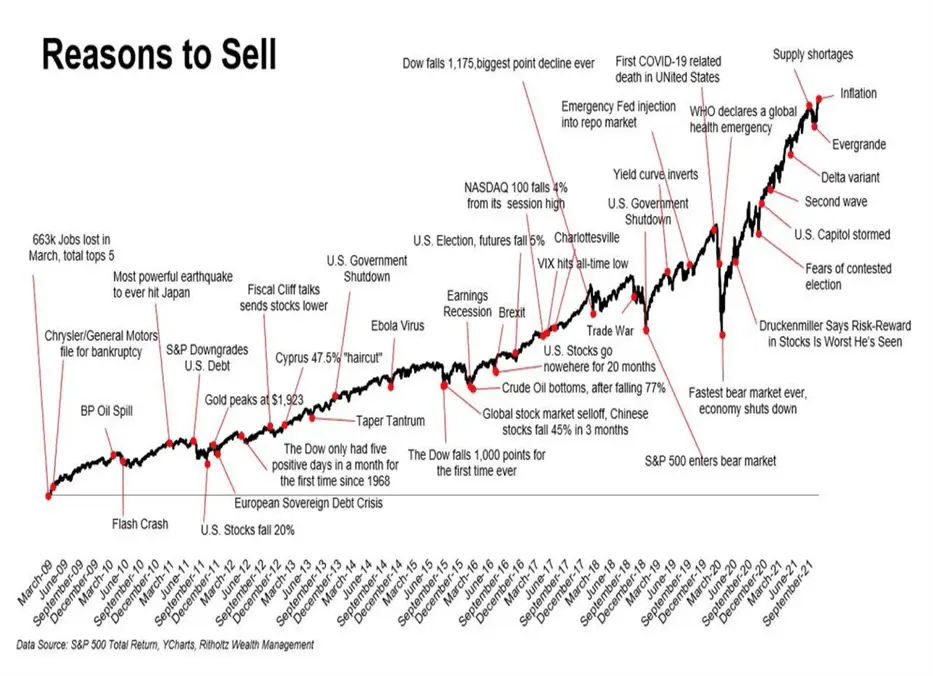

The unfortunate truth is that this inherently human behaviour, and the mistimed selling that ensues, is counterproductive to asset holders. The chart below displays countless supposed “reasons to sell” over the last several years, when the reality is that investing throughout this timeline, and especially during these events, would have proven the most profitable. At Evans, we adopt this philosophy, agreeing with Warren Buffett’s advice to be greedy when others are fearful and fearful when others are greedy.

Timing the market is extremely challenging. Technically, yes, it is true that if you could accurately predict tops and bottoms you would do better than holding through market cycles. But, as Russia found out the hard way in the 19th century, properly timing a sale is difficult. Over the past decade, the S&P 500 index hit new all-time highs roughly 330 times. To consistently “time the market”, one would have needed to time a sale correctly at the top of the market over 300 times and to have bought in again at a lower price before the next climb. The odds of successfully accomplishing this are infinitesimally small. For this reason, at Evans we do not even attempt to time the market, but instead believe long-term success comes from “time in the market.”

In retrospect, the Alaska purchase is often viewed as a shrewd move by the United States, as the territory eventually yielded substantial economic and strategic benefits. It also highlighted the vision of key figures like William H. Seward, who saw the potential value of Alaska when others did not. In contrast, Russia is remembered for selling what would have been a bountiful asset too early. We draw two lessons from this story: first, to look for value where others are not; and, second, to remain invested in the market, not selling during times of market pressure.

THE DEVELOPING INTEREST RATE & INFLATION PICTURE

Since June 30, 2020, the Government of Canada (“GOC”) five-year bond yield has increased from 0.37% to 4.25%. There are several reasons for this (and government bond yields’ in general) rise:

1. Central banks are increasing short-term rates to fight inflation.

2. Security markets are realizing that inflation is “stickier”, in other words less transitory than initially anticipated, meaning interest rates will be higher for longer.

3. The supply of government bonds has been outpacing their demand, with large overseas investors and banks (rumoured to be Russia and China) reducing their U.S. bond holdings, North American central banks reversing their bond purchases from the Covid quantitative easing, and governments borrowing more to fund their growing budgets. With so many fixed income issues to choose from, higher yields are now required to entice investors to buy government bonds.

This quarter, after the pausing of interest rate increases by both Canadian and U.S. central banks, we have begun to see signs of more persistent inflation. In August, the Canadian Consumer Price Index increased to 4%, up from 3.3% in July, driven mostly by increased housing costs and high energy prices. Security markets declined following this news amid the expectation that global central banks may need to cause further economic pain for borrowers by keeping interest rates higher for longer than expected.

We do not base investment decisions on macro forecasts, subscribing as we do to the belief that it is incredibly difficult to predict macroeconomics accurately, and thus it is not a strategy where many can add differentiated value. Most investors famous for their long-term investing success, such as Warren Buffet or Peter Lynch, not only avoid using assumptions that meaningfully deviate from historic macroeconomic averages but also have repeatedly publicly dismissed that those tactics add any value over time. In an interview earlier this year, Howard Marks said it best, if bluntly: “We don’t have many people who got famous or rich from macro forecasting.”

Although higher inflation and a looming recession have created market volatility over the past two years, we continue to see this volatility as presenting opportunities. In stark contrast to the low bond yield environment of the past decade, we are continuing to see bond yields increase. Balanced portfolios (meaning those that hold fixed income securities as well as equities) now look much more attractive than in recent history, and we are finding great value in both equities and fixed income.

WHERE WE CONTINUE TO FIND VALUE

Bonds & Preferred Shares

The earnings yield (earnings ÷ price, or the inverse of the price-to-earnings (“P/E”) ratio) of the S&P 500 is now 5.15%, and many investment grade bonds yield 6% or more. This is a sharp reversal compared to the past few years when bond yields were much lower than the S&P earnings yield. Bonds are once again competitive with stocks as a worthwhile investment.

Our bond portfolio continues to have a low duration compared to the FTSE TMX Universe Bond Index (4.2 vs. 6.9 years), meaning our bond portfolio is less affected by interest rate increases than the index. The yield-to-maturity of our bond portfolio is 7.07% in comparison to 5.16% for the FTSE TMX Universe Bond Index.

As part of our fixed income investments, we also uncover value in preferred shares, particularly for taxable accounts. Dividends from Canadian preferred shares are eligible for the dividend tax credit in non-registered accounts, resulting in a lower tax rate relative to interest income from bonds. We restrict our preferred share exposure to a small portion of the portfolio since they are riskier than bonds, which is a result of the priority ranking of bonds on a company’s assets in the event of default/bankruptcy. We mainly invest in two types of preferred shares: rate reset and floating rate.

Rate reset preferred shares are the most common type of preferred shares in Canada, and typically pay a fixed rate dividend for the first five years after being issued. At the end of the first five years, and every five-year period thereafter, the issuing company can either at their discretion redeem the preferred shares or allow them to remain outstanding. If the preferred shares remain outstanding, a new dividend rate is set for the next five years based on a predetermined spread above the prevailing GOC five-year bond yield. For example, if the predetermined spread on the preferred share is 200 basis points (or 2.00%) and the five-year bond yield is 4.25%, the new dividend rate would be 6.25%. This reset provision gives investors some protection against rising interest rates.

In contrast, floating rate preferred shares pay dividends based on a percentage (70% to 100%) of the prevailing Canadian bank prime rate. Only the issuer has the option to redeem this type of preferred share. The floating dividend rates are reset, and the dividends paid out, either monthly or quarterly.

Inefficiencies in the Canadian preferred share market are currently allowing us to find floating rate preferred shares yielding over 10%, and rate resets at 8% or more. When one adjusts for the difference in tax rates between Canadian preferred share dividends and interest income, the floating rate preferred shares are trading at tax equivalent yields of more than 13% and rate resets in excess of 10%.

We have also been buying a few rate reset preferred shares that are currently yielding only about 6.5%, but their dividend rates are coming up for reset within the next nine months. With the GOC five-year bond yield where it is today, the dividend rates look to reset well above their current level, which will result in much higher yields. This provides for the opportunity for capital appreciation, as investors will eventually move to the higher yielding preferred shares.

Overall, we are finding significantly more value in fixed income securities than we have in the past five years and are more excited about the traditional “Balanced” portfolio (i.e., 60% equities/40% fixed income) than we have been in recent history.

Spin Master Corp. (TOY)

We continue to find value in equities like Spin Master Corp. , a Canadian multinational toy and entertainment company. In 1994, Spin Master was founded in Toronto by three childhood friends. Over time, the friends grew the business to be an industry leader in the toy space, both through internally developed toys and well-executed strategic acquisitions. Today, Spin Master engages children everywhere through brands and products like Paw Patrol, Bakugan, Rubik’s Cube, Hatchimals, and many more.

*Some clients might not hold Spin Master due to asset mix or timing.

Since its initial public offering or “IPO” in 2015, Spin Master had amassed a premium multiple to the market (about 18 times price to the next-twelve-months’ earnings per share), due to its innovation in toy products, intelligent acquisitions, and strong balance sheet. These factors have led to an impressive 25% earnings per share compounded annual growth rate since its IPO. Although these fundamentals continue to be true, the stock’s price has recently been punished, most likely from fears that a cyclical toy industry will hurt Spin Master’s earnings in the near term. Now trading at just 12 times 2023 price-to-earnings, Spin Master is expected to produce cash flow equal to roughly 8% of its current market value this year. In addition, the company currently boasts a net cash balance sheet position of $6.23/share (which is 18% of the current share price of $34.15). Compared to its more leveraged and mature peers, Mattel and Hasbro, which trade at 18 times and 15 times 2023 price to earnings, respectively, we think Spin Master is inexpensive, stronger financially, and offers greater opportunity for growth.

Recently, Spin Master decided to put its cash to work. On October 11, 2023, they agreed to buy children’s toy producer Melissa & Doug for $950 million (deal expected to close in Q1 2024). Melissa & Doug’s portfolio of toys for children aged 0-8 should complement and expand Toy Master’s portfolio. The transaction will be financed by $450 million in cash and $500 million in debt. We are excited to see Spin Master is still playing offense and using acquisitions to expand their market share in the child entertainment space.

In addition to further product innovation and strategic acquisitions, future growth potential might come from Spin Master transitioning to a franchise model, similar to what Disney did with Marvel and Star Wars. Over time, Spin Master has diversified into media and video games using brands that they have built internally. The most recent success story has been Paw Patrol, which has ranked as the top preschool series for the last ten years. In 2021, Spin Master released the first Paw Patrol movie with a budget of US$26 million. It which grossed US$150 million in theatres. The final weekend of September 2023, the second Paw Patrol movie was released, grossing US$46 million its opening weekend on a budget of US$30 million. Branching out into a franchise model around brands with cross-selling capabilities in video games, media, and toys could provide further upside potential for the company.

As we have done for over 35 years, we continue to find great value for clients by thinking long term and being judicious when others are acting emotionally. Our portfolios are well-positioned relative to the market: we hold companies that are less leveraged, more profitable, and faster growing. We continue to put our clients first in every decision we make, to ensure their prosperous financial future.

Thank you for your continued confidence and support.

The Evans Team