| Index | Q3 2024 | YTD |

|---|---|---|

| S&P/TSX Composite (C$) | 10.5% | 17.2% |

| S&P 500 (US$) | 5.9% | 22.1% |

| S&P 500 (C$) | 4.4% | 24.6% |

| MSCI EAFE (US$) | 7.3% | 13.0% |

| MSCI EAFE (C$) | 5.8% | 15.3% |

| FTSE TMX Universe Bond Index (C$) | 4.7% | 4.3% |

| C$ / US$ | 1.3687 to 1.3499 (1.4%) | 1.3226 to 1.3499 (-2.0%) |

* Index returns are total returns, including dividends.

FARAWAY LANDS

“In love of home, the love of country has its rise.” – Charles Dickens

As humans, “home” makes us feel safe and secure. It makes us feel protected from storms and those who wish us harm. It provides an environment for love and family. This innate instinct dates back millennia. Interestingly, as cultures and borders formed, this sense of home began extending to one’s own country – and with it, national pride was born.

In investing, “home country bias” is a principle explaining the way most investors tend to prefer investing in companies based in their own country. For example, a Vanguard study conducted in 2022 indicated that 52% of Canadians’ stock holdings are in Canadian companies. This is much higher than Vanguard’s suggested “optimal” weight of around 30%, and Canada’s 2% contribution to global Gross Domestic Product (“GDP”).

In addition to portfolio security weightings, home country bias can also cause Canadian investors to focus on Canadian or, more broadly, North American news and economic data. While of course it is important to look at trends and macroeconomic data at home and very close to home, an overemphasis on it can cause an investor to miss exciting opportunities abroad. However, in the spirit of national pride, let’s discuss for a moment the current economic climate Canada is facing.

Canada’s most recent inflation reading was 2%, exactly in line with its target of 2%. This followed three Bank of Canada interest rate cuts of 0.25% each, bringing the Bank of Canada’s interest rate down to 4.25% from a 22-year peak of 5%. This is high compared to recent history, and above the 30-year average of 2.6%. Remember that interest rates were originally increased to 5% in 2022 and 2023 to slow the economy down by increasing borrowing expenses for businesses and individuals, and in turn combat the high inflation Canada was seeing in 2021 and 2022. Today, the Bank of Canada is walking a fine line between lowering interest rates too quickly at the risk of reigniting inflation, or bringing them down too slowly and sending the country tilting into a bad recession.

Our neighbours to the South are walking a similar tightrope. Although America’s economic output (GDP) has been stronger than ours, inflation is coming down to its target rate more slowly. As a result, the Federal Reserve (the U.S. version of the Bank of Canada) decided to maintain its policy interest rate at 5.5% until September, at which point it was lowered to 5%.

By now, your brain might have already started going down a rabbit-hole of predicting Canada’s economic outlook or guessing when the next U.S. interest rate cut might be. We’re going to challenge you to think like Ferdinand Magellan or Marco Polo and explore the rest of the world instead. Fixating on Canadian or American securities, although it may carry some tax benefits, can lead to missing some great investment opportunities abroad – especially in today’s environment.

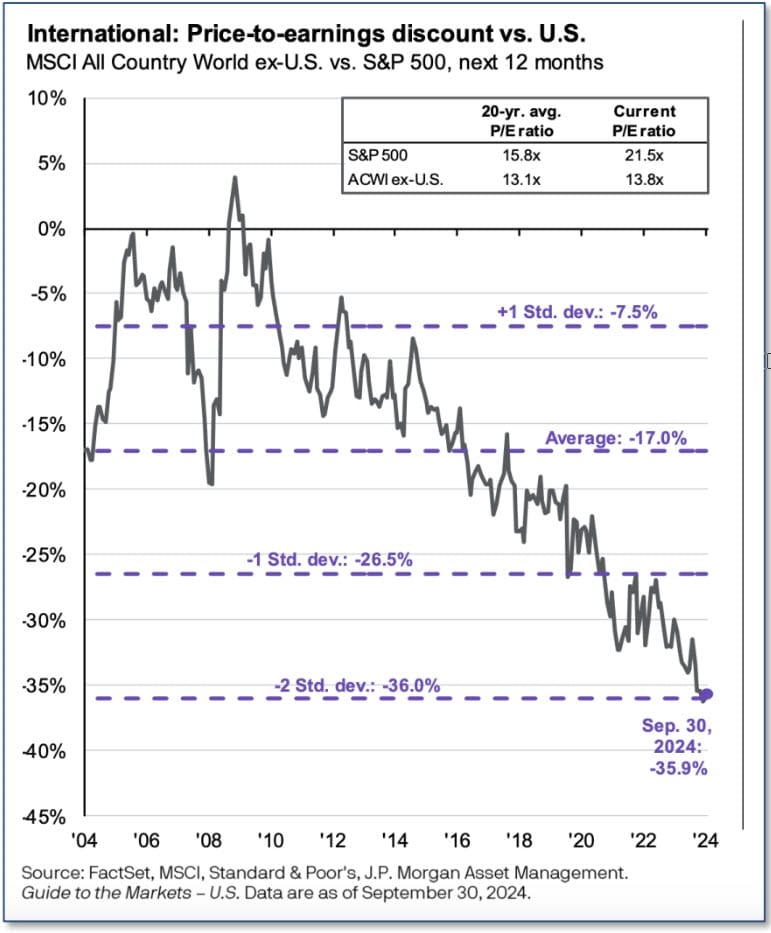

It is true that the U.S. equity, more specifically the S&P 500 and the NASDAQ, have had incredible runs over the past decade, and we will certainly continue to maintain heavy exposure to this market. However, the disparity between U.S. and International markets is now uncharacteristically high (as shown below). International markets have become a rich hunting ground for inexpensive equities with similar qualities to U.S. companies.

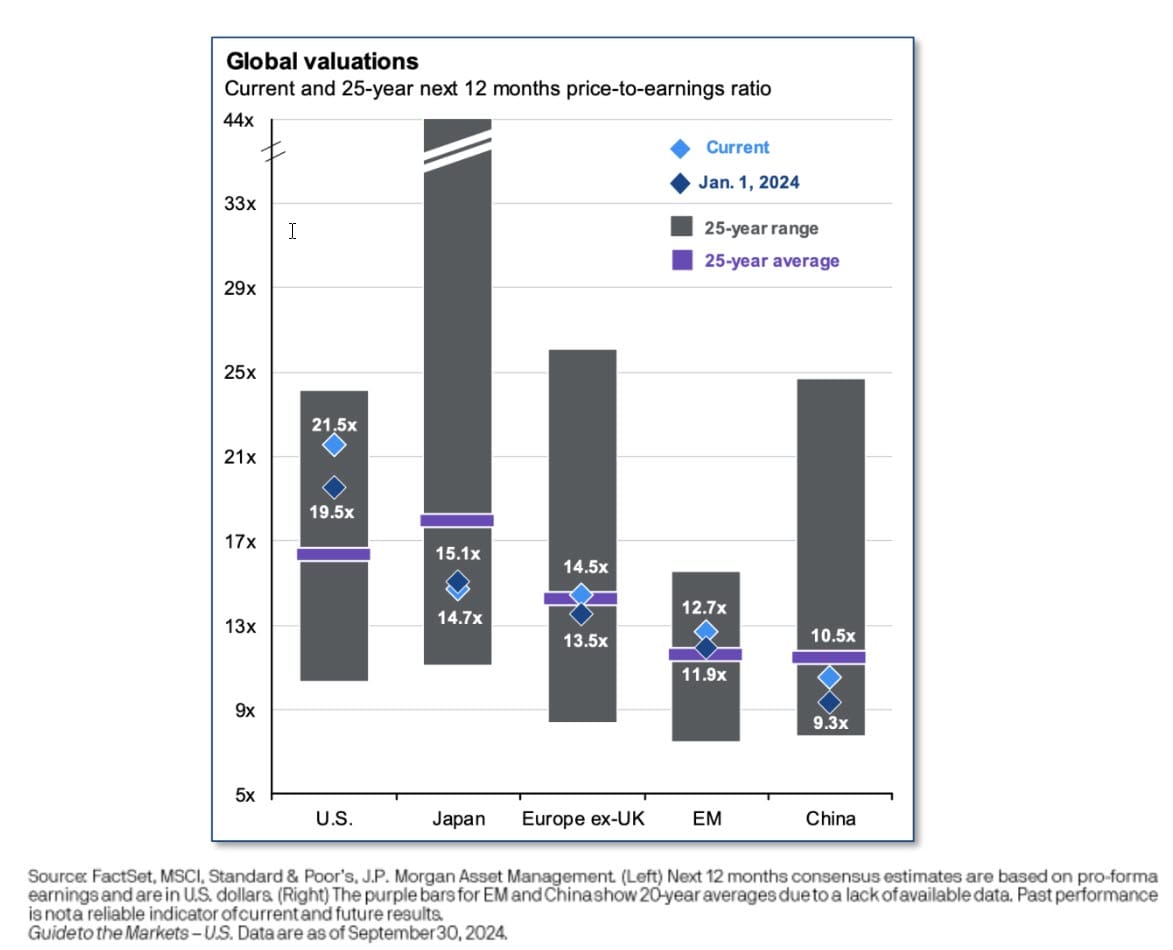

The second chart (below) shows pockets outside the U.S. stock market where good value can be found. As you can see, Japan, Europe (ex-UK), and China are all trading at or below their historic average price-to-earnings ratio (“P/E”) and well below the high end of their 25-year range. Compare this to the U.S. equity market, whose P/E is significantly above its historic average and towards the higher end of its 25-year range. In addition, its valuation is higher than the other markets on an absolute value. If you can find similar quality companies to invest in – and pay up to 50% less for them – wouldn’t you want to do so, even if the companies are from a different part of the world? For example, Amazon is an incredible American company, but it is currently trading at an eye-watering 39x P/E. Compare this with Alibaba, a Chinese company similarly dominant in its market and just as focused on online retail, Cloud hosting, and Artificial Intelligence. It trades at 13x P/E (67% less than its American peer). Another example is Ford, an American car manufacturer responsible for the Ford, Lincoln, and Troller brands, which currently trades at 5.7x 2025 P/E. Contrast that to Stellantis, a European car manufacturer responsible for the Fiat, Chrysler, Ram, Jeep, Dodge, Maserati, and Peugeot brands, which currently trades at 3.6x 2025 P/E – a 37% discount compared to its American counterpart.

Of course, it would be naive not to recognize the risks that come with international investing. First, being halfway across the world, it is more difficult for our investment team to understand the quality of some of these businesses since we don’t have “boots on the ground” familiarity and experience. In addition, the rule of law may be different in some of these countries, and incentives may not be as strongly aligned to business formation as in the U.S., making these businesses less competitive on a global scale. Lastly, there is geopolitical risk, especially for countries such as China.

All these factors pose real risks, but consider that at the end of Q3, Chinese equities began showcasing what can happen when there is even a slight reprieve of geopolitical risk. The Chinese government recently proposed economically friendly policies, and Chinese stocks have since soared because of it: many Chinese equities gained up to 50% in a matter of weeks. Stock prices there are still far from their all-time highs, but they are still a reminder of just how inexpensive some of these securities had gotten, and how quickly they can gain momentum when the tides turn.

As Canadian investors, we will continue to lean towards North American securities, taking advantage of more favourable tax treatment, closer proximity to the products and management, and a business-friendly economic and legal system. However, we will also continue to explore new opportunities wherever they can be found, and make sure that our home country bias does not prevent us from uncovering phenomenal investment opportunities overseas.

VALUE IN A RICHLY VALUED MARKET

Global Payments Inc. (1) (“GPN”) is an American-based provider of payment technology and software solutions. It was founded in 1967 as part of National Data Corporation (“NDC”), focusing on electronic payment processing. It became an independent company in 2001 when it was spun out of NDC and began trading at US$3.75 per share on the New York Stock Exchange. Today, the stock is trading at just under US$100 per share and the business has grown from US$350 million revenues in 2001 to over US$9 billion last year (a 16% compound annual growth rate).

Global Payments processed over US$1 trillion worth of purchases for its customers last year. Its payment system is global in scale, with physical operations in 38 countries, although 80% of its revenue comes from the U.S. (with the rest mostly from Europe, Canada and Australia). As a Canadian you might best recognize its brand Verifone, if not the name of the company itself. It offers a wide array of solutions including payment processing, settlements, POS terminals, system integration, payroll, inventory and other software services like loyalty programs, appointment scheduling and reservations. On average, it makes about 0.5% per transaction, but this can vary significantly depending on the size of the merchant and the type of transaction (online vs offline).

Global Payments serves two customer types: Merchants (77% of revenue) and Issuers (23% of revenue). For its Issuer customers, like PayPal, it processes 35 billion transactions annually for 830 million underlying customers and make most of its revenue (70%) selling software solutions. In Merchants, it serves over 1 million businesses at 5 million locations who range in size from

Domino’s, Tim Hortons and Starbucks all the way down to your local dentist, veterinarian, or family- run restaurant. Its customer base is very diversified, with much of its revenue coming from small- and medium-sized businesses in the retail, healthcare, and restaurant sectors.

The stock has corrected significantly from 2021, when the price peaked at US$220 a share. GPN now trades at 8x P/E compared to the S&P 500 Index at 22x and its closest peers Fiserv (21x) and Fidelity National (17x). Since it began trading in 2001, Global Payments has averaged a P/E of 18x and has never been cheaper than it is today (currently at a 55% discount to its historical average). Global Payments is inextricably tied to consumer spending which will, at the very least, grow with inflation. We believe it should also benefit from the further transition of consumers in America to credit cards from cash: in 2023, Americans used credit cards for just 76% of consumer-to-business transactions – a number we expect will continue to increase over time (in Canada it is over 90%). At its investor day in September, Global Payments announced a US$7 billion capital return plan over the next three years. Given its current market capitalization of US$25 billion, this suggests it will repurchase at least 7% of its own stock annually. Between the minimum growth rate and the capital return, we expect a double-digit return on the stock from here, with further upside due to stronger growth from geographic or market-share expansion (over the past three years, top-line growth has been 9% per year). Alternatively, we could see its P/E multiple re-rate higher, which is currently two standard deviations below the mean.

(1)Some clients might not hold Global Payments due to asset mix or timing.

EXPANDING OUR BOND PORTFOLIO

We are also finding good value in fixed income markets with securities like Athabasca Oil’s 2029 bonds (2) . Athabasca Oil is a Canadian energy company primarily focused on the exploration and development of oil sands and the production of light oil in the province of Alberta. It was founded in 2006 and has its headquarters in Calgary, Alberta.

Historically, Canadian oil exploration and production (“E&P”) companies have only offered bonds denominated in U.S. dollars. Since we typically only buy bonds denominated in Canadian dollars to avoid taking on foreign-exchange risk for our Canadian clients, this generally prevented us from owning bonds of Canadian oil E&P companies. However, their recent choice to issue bonds in Canadian dollars helps us fill a gap in our portfolios that we had long lamented.

We believe that Athabasca gets an unjust and punitive B+ bond rating (considered non-investment grade, speculative, high yield, or junk bond on the bond rating scale) due to the industry in which it operates (oil and gas) and its small size (market value of only $3 billion) versus its competitors. As a result, the bond offers what we deem is a compelling 6.75% coupon rate and trades at roughly $101, implying a yield-to-maturity of 6.5% with a 3.75% spread over a Government of Canada bond of the same maturity.

We firmly believe that Athabasca’s credit rating of B+ is harsh relative to the risk in the company. Although Athabasca operates in a cyclical industry, it has a strong balance sheet and generates significant cash at current oil prices. In 2024, Athabasca’s management team expects the company to generate $350 million in free cash flow, compared to its $233 million in debt obligations. Think about it: if your kids borrowed $100 from you to open a lemonade stand, and after one year the stand had produced $150 in cash, you would feel pretty confident you’d get your money back, wouldn’t you? In addition, the company has $125 million of net cash (that is to say, cash over and above its debt obligations of $233 million) as a buffer if it begins to lose money in a down cycle, adding another layer of safety.

As always, we look for value where it can be found. We are careful not to get caught up in runaway markets and are prudent about the price we pay for securities. This prudence may take us to the unloved areas of North American markets to find reasonably priced securities, or even abroad. However, in the end, we are generally unconcerned where the opportunities come from, as long as they provide a favourable return in exchange for the risk we are taking. That’s what we have always – and will always – search for.

(2) Some clients might not hold Athabasca bonds due to asset mix or timing.

Thank you for your continued confidence and support.

The Evans Team